Research on Use Motivations of Mobile Payment Adopters: A Case Study on Chinese Oversea Students in South Korea

1)

전체 글

1)

수치

관련 문서

In terms of the relationship between personal service contact and passengers' emotions, this study classified service contact quality factors into four groups based on

The IASCF reserves all rights outside of the Republic of Korea and in any use other than use of the above materials in the Korean language by any

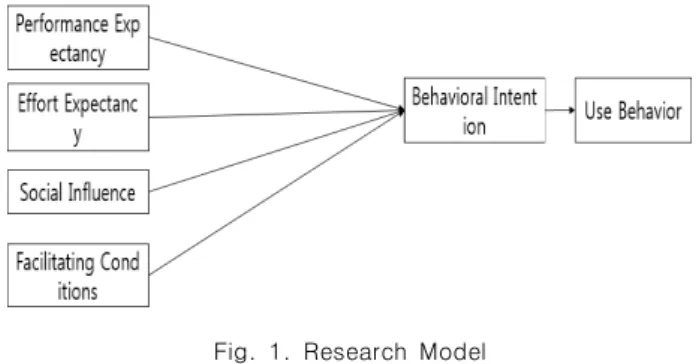

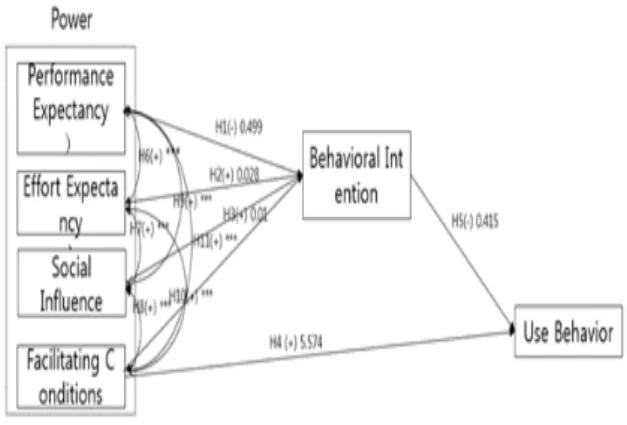

This research focuses on investigating the main factors on using behavior and using intention of mobile payment service, and provides basic materials related

This paper proposes a perspective of political economy to explore important issues on regulation studies, focusing on the case of tobacco control in South

This paper proposes a perspective of political economy to explore important issues on regulation studies, focusing on the case of tobacco control in South Korea.

adio Frequency Identification Tech- nology (RFID) is the state-of-the-art information and communication tech- nology(ICT) that uses radio waves for

1 John Owen, Justification by Faith Alone, in The Works of John Owen, ed. John Bolt, trans. Scott Clark, "Do This and Live: Christ's Active Obedience as the

We’re going to use the special init function (in both our Model and our ViewModel) We’re going to use generics in our implementation of our Model. We’re going to use a function