56-1 / S. Jung

IMID 2009 DIGEST •

Abstract

Conversion of light energy to electrical energy by using a solar cell has long been considered as one of the option for an electrical energy supply in the future. In the past, commercial use was restricted largely to remote area applications where conventional electricity is expensive. Recently, the major application of the solar cells changed to become generation of residential electricity in urban areas where the electricity is already supplied by the conventional grid. This paper covers the current market and technology status of the solar cells and future prospect of their terrestrial applications. Reviewing market trend, this paper discusses high efficiency approach in silicon solar cells, low cost approach in silicon solar cells and finally covers future prospects of silicon solar cells.

1. Objectives and Background

Improvement in the cell economics and the accelerating interest of the global community in sustainable energy generation is driving force for this transformation. Rapid depletion of the fossil fuel resources and their price hike due to different wars in the world at different times forced the whole world to consider the PV energy as a renewable energy in the years to come. Viewing from another aspect, the environmental degradation is the hot issue of our age. The means of generating energy from different existing resources are the major threats to our degrading environment. In this context, solar cell technology can kill three birds (economy recession, energy crisis and environmental degradation) with one stone. However, it is also a great challenge for manufacturer, researcher and the scientific community as a whole to make it widely popular and acceptable source of energy despite its higher cost of installation compared to other existing resources of energy at the moment. This paper discusses the current status of the solar cells in terms of country, material, market, industrial technology and future prospect of their terrestrial applications.

2. Current Status of the Market

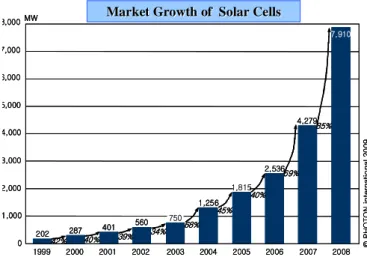

The world market for the PV products has been expanding with a high growth rate of 85% in 2008 (7.9 GW solar cell productions) [1]. The producer and consumer of the photovoltaic products can be categorized mainly into four sectors viz. Japan, USA, China, Europe and rest of

the world. This could be mainly due to several factors such

as the technological advancement brought up by massive research and development, huge investment for the new manufacturing plants, cost reduction with the use of new materials and the pressurizing international agreements in environmental protection. Q-Cells based in Germany is the world’s largest manufacturer of photovoltaic cells with total power generation of 582 MW per annum. USA based company First Solar, the world’s second largest manufacturer of photovoltaic cells, produced over 500 MW in the year of 2008. China based company Suntech Power the third largest amount of 497MW last year. There are three among top ten largest companies of the world in Japan; Sharp (473 MW), Kyocera (290MW) and Sanyo (215MW). 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 202 287 401 560 42% 40% 39% 34% 750 68% 1,256 45% 1,815 40% 2,53669% 4,27985% 7,910 MW © PH OT ON in te rn a ti o n a l 2 0 0 9 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 202 287 401 560 42% 40% 39% 34% 750 68% 1,256 45% 1,815 40% 2,53669% 4,27985% 7,910 MW © PH OT ON in te rn a ti o n a l 2 0 0 9

Market Growth of Solar Cells

Market Growth of Solar Cells

Fig. 1. World PV market growth over the last decade.

Current Status and Future Prospect of Terrestrial Solar

Cell Applications

Sungwook Jung

1,2, Youngkuk Kim

1,2and Junsin Yi

1,21

School of Information and Communication Engineering, Sungkyunkwan University, Suwon, 440-746, Korea

TEL:82-31-290-7139, e-mail: [email protected]

2

Dept. of Energy Science, Sungkyunkwan University, Suwon, 440-746, Korea Keywords : Solar Cell, High Efficiency, Low Cost,

56-1 / S. Jung

• IMID 2009 DIGEST

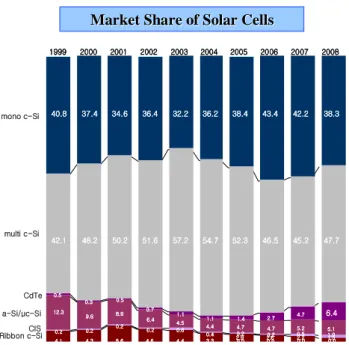

Material-wise market shares are mono-crystalline silicon=38.3%, multi-crystalline silicon=47.7%, cadmium telluride (CdTe)=6.4%, Thin film silicon=5.1%, copper indium diselenide (CIS) film=1.0%, Silicon sheet=1.5%. The study of Solar cell materials indicates that 93% of market is occupied by silicon source. A commercial silicon solar cell of 20 % efficiency is not a surprise at all these days. The solar cell made of crystalline silicon is the most popular and the successful at present. Screen printed metal contact technology dominant in the current crystalline silicon solar cell market.

mono c-Si multi c-Si CdTe a-Si/μc-Si CIS Ribbon c-Si 40.8 37.4 34.6 36.4 32.2 36.2 38.4 43.4 42.2 38.3 40.8 37.4 34.6 36.4 32.2 36.2 38.4 43.4 42.2 38.3 42.1 48.2 50.2 51.6 57.2 54.7 52.3 46.5 45.2 47.7 42.1 48.2 50.2 51.6 57.2 54.7 52.3 46.5 45.2 47.7 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 0.5 0.3 0.5 0.7 1.1 1.1 1.4 2.7 4.7 6.4 12.3 9.6 8.9 6.4 4.5 4.4 4.7 4.7 5.2 5.1 0.2 0.2 0.2 0.2 0.6 0.4 0.2 0.2 0.5 1.0 4.1 4.3 5.6 4.6 4.4 3.3 2.90.0 2.60.0 2.20.0 1.50.0 0.5 0.3 0.5 0.7 1.1 1.1 1.4 2.7 4.7 6.4 12.3 9.6 8.9 6.4 4.5 4.4 4.7 4.7 5.2 5.1 0.2 0.2 0.2 0.2 0.6 0.4 0.2 0.2 0.5 1.0 4.1 4.3 5.6 4.6 4.4 3.3 2.90.0 2.60.0 2.20.0 1.50.0

Market Share of Solar Cells

Market Share of Solar Cells

Fig. 2. Material-wise market shares over the last decade.

3. High Efficiency Approach for Crystalline

Silicon Solar Cells

Three companies of the world are coming up with three different modifications in the first generation cells for the high efficiencies. Sanyo is still in the leading position with the latest version of Heterojunction having intrinsic thin-layer (HIT) cells and modules with the conversion efficiency of 20% in its commercial production and a cell of 22% efficiency is reported to have been fabricated in their laboratory[2]. Similarly, the second company in the race of high efficiency commercial cells is BP-solar, which has been manufacturing the laser grooved buried contact solar cell ( BCSC) taking a silicon wafer of size 125 mm x 125 mm. It is capable of achieving a cell with 19% efficiency using laser grooved buried metal contact instead of conventional screen printed metal contacts[3,4]. SunPower of USA is coming up in the market with the cells having contacts only at the back surface (Back Integrated Cell) as the number one company in the race of high efficiency cells. Sun Power Company is expected to enter into the

competitive world market with its cells of efficiency over 22%, fabricated with FZ-silicon instead of traditional CZ – silicon[5]. Longer Process Pure Si Wafer Need BetterIso. Longer Process More Fab.Steps More Metal steps Large Investment Need Better FF for Large Area

Cons R&D: 22% Product: 20% Low Cost Module Process SunPower (BIC) SiO2/N+/n-type FZ or CZ, 200μm/p+/Cu/Sn n+/Cu/Sn R&D: 22% Product: 18% Thin Wafer Large Area P-type wafer BP (BCSC) Ag/Cu/ Ni/n+/ CZ p-type, 240μm/ /P+/Al/Ni/Cu/Ag R&D: 21% Product: 17% Low Temp. Use of a-Si:H Cell Line Sanyo (HIT)

P+/i type a-Si:H/ CZ n-type, 200μm/

i/n+ type a-Si:H

Note Pros

Structure Pros & Cons Company Longer Process Pure Si Wafer Need BetterIso. Longer Process More Fab.Steps More Metal steps Large Investment Need Better FF for Large Area

Cons R&D: 22% Product: 20% Low Cost Module Process SunPower (BIC) SiO2/N+/n-type FZ or CZ, 200μm/p+/Cu/Sn n+/Cu/Sn R&D: 22% Product: 18% Thin Wafer Large Area P-type wafer BP (BCSC) Ag/Cu/ Ni/n+/ CZ p-type, 240μm/ /P+/Al/Ni/Cu/Ag R&D: 21% Product: 17% Low Temp. Use of a-Si:H Cell Line Sanyo (HIT)

P+/i type a-Si:H/ CZ n-type, 200μm/

i/n+ type a-Si:H

Note Pros

Structure Pros & Cons Company

Fig. 3. The first generation cells for the high efficiencies.

4. Low Cost Approach for Silicon Solar Cells

The cost of silicon wafer takes over 60% of the total manufacturing cost of a cell. Multi-crystalline silicon could reduce material cost over 30% in comparison to that of single crystalline silicon. However, poor material quality of multi-crystalline silicon illustrated a low minority carrier lifetime due to increased recombination rate in crystalline defects. Numerous technical investigations such as surface passivation, optimal doping, gettering, selective emitter, anti-reflection coating, novel texturing, and screen printing, local contact, rapid thermal anneal, back surface field and cell structure were carried out to overcome the shortcomings of multi-crystalline silicon. Now, industries have achieved the established cell fabrication process optimization to give similar conversion efficiency like screen printed single crystalline efficiency about 16% for the mc-Si solar cell too. The recent demonstration of 20.3 % cell efficiency for a small area multicrystalline cell suggests some of the potential lying in this area [6]. Future material and solar cell cost reduction approach could be forecasted in two categories. The first one is the use of thin wafers with 100 µm thickness, which requires a new type of cell fabrication technology. This approach is expected to dominate the solar cell market within 5 years. Companies like Astropower (Silicon sheet), RWE (EFG), Evergreen (string ribbon) have already expanded their market shares with thin wafer approach. Other companies want to make use of thin wafer prepared by using a multi-wire saw cut. The second one with the long term future of solar cells that is likely to be decided within a decade from now. It is believed to be based on what is known as a "thin film" technology. In the thin film approach, a thin layer of the photovoltaically active material is deposited onto a supporting substrate or superstrate. This approach not only greatly reduces the semiconductor material content of

56-1 / S. Jung

IMID 2009 DIGEST • the finished product (over 100 times less material) but also

allows for higher throughput in the commercial production since the module, instead of the individual cell, will be the standard unit of production (a unit some 100 times larger unit). There are cell manufacturing technologies based on many competitor materials such as hydrogenated alloy of

thin film of amorphous silicon, compound semiconductor such as copper indium diselenide, cadmium telluride, nanocrystalline titanium dioxide and polycrystalline silicon. One type of thin film cell is based

on a hydrogenated alloy of amorphous silicon, as successfully commercialized by Japanese companies particularly for consumer products such as pocket calculators and digital watches. The second is based on the use of the compound semiconductor, copper indium diselenide. This approach has produced the highest laboratory performance for thin film cells with small area devices giving efficiency above 19% but has presented manufacturing difficulties. The third is technology based on cadmium telluride, which has been proved to be very robust from the manufacturing point of view. CdTe cell

may occupy the number one production capacity in 2009. The fourth is a unique technology based on a

nanocrystalline titanium dioxide in combination with organic dyes that were initially developed in Switzerland. The fifth is based on thin films of polycrystalline silicon, very similar material to the one which is popular in the commercial market of the present day. Therefore, the polycrystalline silicon film has an advantage over rest of the materials. Since the thickness of the semiconductor material required in the film may only be of the order of 1 micron, all the semiconductor materials will be inexpensive to be a candidate for solar cells. Silicon is one of the few those cheap materials to be used as a self-supporting wafer based cell. Many semiconductors that have been investigated with those five thin film technologies are now the focus of research and development for commercial production.

Solar Cells from Direct Wafer Growth (Mass Production/R&D)

Solar Cells from Direct Wafer Growth (Mass Production/R&D)

Fig. 4. Low Cost Approach for Silicon Solar Cells

5. Future Prospect of Solar Cell Industry

It is clear that terrestrial solar cell application in the residential houses of urban areas, public buildings, schools, apartment complexes will become a dominant application area. Many nations such as Japan, China, USA, Germany, Italy, Austria and EU have already initiated solar roof-top applications. Japanese exploration of the technical issues relevant to residential use has been followed by a similarly steady market development exercise. Looking at the overall trend of the solar cells at present, we can outline the future track of the solar cell world. The process of transformation from the first generation to second generation solar cell should be geared up with the entry of new approaches but still silicon seems remains as the major material for solar cells for many years to come. Market force, industries as well Research and Development teams must usher the new areas with the encouraging policies and the subsidies from the governments of the global community for the innovative approach of high efficiency, low cost solar cells. This is how we can promise people of the third millennium for a clean and sustainable substitute for the depleting and pollution conventional non-renewable energy resources.

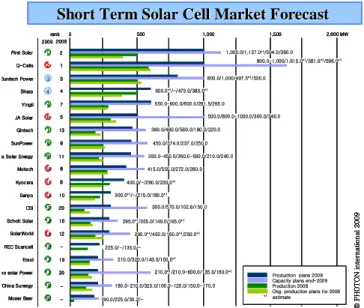

rank 2009 2008 2 -© P H O T O N i n te rn at io n a l 2009 3 1 2 4 1,000.0/1,127.0*1/504.0/390.0 First Solar 1 Q-Cells 3 Suntech Power 4 Sharp 4 6 7 Yingli 5 JA Solar 7 13 Gintech 8 9 SunPower 8 11 a Solar Energy 10 8 Motech 11 6 Kyocera 12 10 Sanyo 12 20 CSI 14 16 Schott Solar 15 12 SolarWorld 16 -REC Scancell 17 19 Ersol 17 20 eo solar Power 19 China Sunergy -20 Moser Baer 0 500 1,000 1,500 2,000 MW 800.0-1,000/1,615.0*1/581.6*1/596.0*1 800.0/1,000/497.5*1/530.0 600.0*1/-/473.0/380.0*1 550.0-600.0/600.0/281.5/265.0 500.0/800.0-1000.0/300.0/340.0 360.0/460.0/560.0/180.0/220.0 450.0/574.0/237.0/250.0 350.0-450.0/350.0-550.0/210.0/240.0 415.0/555.0/272.0/280.0 400.0/-/290.0/230.0*1 300.0*1/-/215.0/180.0*1 300.0/570.0/102.8/150.0 295.0*1/355.0/149.0/165.0*1 290.0*1/450.0/190.0*1/250.0*1 225.0/-/135.0/-210.0/320.0/143.0/150.0*1 210.0*1/210.0-600.0/135.0/160.0*1 180.0-210.0/320.0/100.0-120.0/150.0-170.0 190.0/225.0/30.2/-Production plans 2009 Capacity plans end-2009 Production 2008 Orig. production plans for 2008 *1estimate rank 2009 2008 2 -© P H O T O N i n te rn at io n a l 2009 3 3 1 1 2 2 4 4 1,000.0/1,127.0*1/504.0/390.0 First Solar 1 Q-Cells 3 Suntech Power 4 Sharp 4 4 6 6 7 Yingli 5 JA Solar 7 7 13 Gintech 8 8 9 SunPower 8 8 11 a Solar Energy 10 10 8 Motech 11 11 6 Kyocera 12 12 10 Sanyo 12 12 20 CSI 14 14 16 Schott Solar 15 15 12 SolarWorld 16 16 -REC Scancell 17 17 19 Ersol 17 17 20 eo solar Power 19 19 China Sunergy -20 20 Moser Baer 0 500 1,000 1,500 2,000 MW 800.0-1,000/1,615.0*1/581.6*1/596.0*1 800.0/1,000/497.5*1/530.0 600.0*1/-/473.0/380.0*1 550.0-600.0/600.0/281.5/265.0 500.0/800.0-1000.0/300.0/340.0 360.0/460.0/560.0/180.0/220.0 450.0/574.0/237.0/250.0 350.0-450.0/350.0-550.0/210.0/240.0 415.0/555.0/272.0/280.0 400.0/-/290.0/230.0*1 300.0*1/-/215.0/180.0*1 300.0/570.0/102.8/150.0 295.0*1/355.0/149.0/165.0*1 290.0*1/450.0/190.0*1/250.0*1 225.0/-/135.0/-210.0/320.0/143.0/150.0*1 210.0*1/210.0-600.0/135.0/160.0*1 180.0-210.0/320.0/100.0-120.0/150.0-170.0 190.0/225.0/30.2/-Production plans 2009 Capacity plans end-2009 Production 2008 Orig. production plans for 2008 *1estimate

Production plans 2009 Capacity plans end-2009 Production 2008 Orig. production plans for 2008 *1estimate Short Term Solar Cell Market Forecast

Short Term Solar Cell Market Forecast

Fig. 5. Short-term solar cell market forecast.

Acknowledgements

This research was supported by WCU(World Class University) program through the Korea Science and Engineering Foundation funded by the Ministry of Education, Science and Technology (R31-2008-000-10029-0).

56-1 / S. Jung

• IMID 2009 DIGEST

References

1. Photon International, 172 March (2009).

2. Yasufumi Tsunomura, Yukihiro Yoshimine, Mikio Taguchi, Toshiaki Baba, Toshihiro Kinoshita, Hiroshi Kanno, Hitoshi Sakata, Eiji Maruyama, Makoto Tanaka, “Twenty-two percent efficiency HIT solar cell” Solar Energy Materials & Solar Cells, (2009).

3. M. A. Green, “ Silicon Solar Cells: Advanced Principles and Practice”, Bridge Printery, Sydney, (1995)

4. J. Zhao, A. Wang, M. A. Green, “19.8% efficient honeycomb textured multicrystalline and 24.4 % monocrystalline silicon solar cell”, Applied Physics Letters;

73: 1991-1993 (1998)

5. R. Swanson, Phtotovoltaics: the path from niche to mainstream supplier of clean energy, PV Equip. Conf. Germany, (2007).

6. J. Yi, Introduction to Solar Cell Engineering, DooYangSa, (2008)