Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi:10.13106/jafeb.2021.vol8.no1.247

The Effect of Intellectual Capital and Financial Services Knowledge on Financial Inclusion

Mar’a Elthaf ILAHIYAH

1, Noorlailie SOEWARNO

2, I Made Laut Mertha JAYA

3Received: September 30, 2020 Revised: November 22, 2020 Accepted: December 05, 2020

Abstract

The study aims to determine the influence of intellectual capital and education on public financial services in increasing financial inclusion.

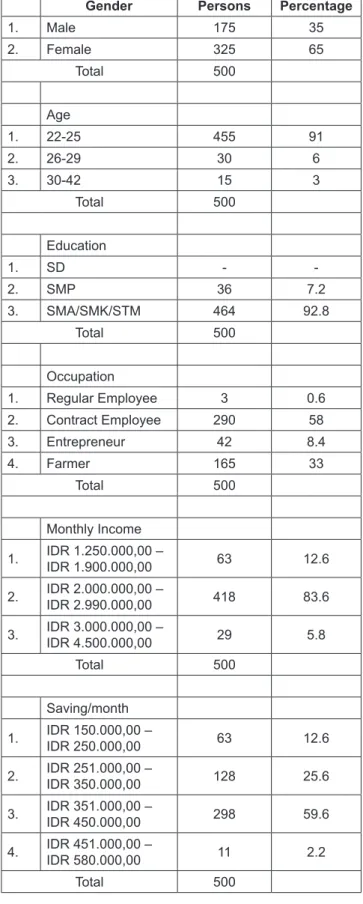

This study applied a survey technique by selecting respondents according to the purposive sampling method. The number of respondents in this study was 500 people and came from various regions in Indonesia. Data analysis was performed using Structural Equation Modeling (SEM) techniques. The results indicate that intellectual capital has a positive effect on financial inclusion. Conversely, education about public financial services has no influence in increasing financial inclusion. The results of this study indicate that the success of financial inclusion programs in Indonesia is caused more by the role of public intellectual capital. Studies show that the public does not have the courage to be involved in banking institutions because the image of this institution tends to be inflexible in its operations. The results of this study are expected to make a real contribution, especially for the government and banks, that in order to achieve the success of the financial inclusion program in Indonesia; the related parties should educate the public directly to citizens who have not been reached by banking services continuously and with a more down to earth approach.

Keywords: Intellectual Capital, Public Financial Service Education, Financial Succession, Unbanked Citizens, Indonesia JEL Classification Code: G28, I22, I25, P46

world, one of which is in Indonesia (Jaya, 2019). Unbanked people are citizens who do not have bank accounts, so they do not have access to any financial services. Previous studies have proven that the financial inclusion program has a significant impact on economic growth, poverty alleviation, income inequality, and financial stability (Cavoli, Gopalan, & Rajan, 2020; Omar & Inaba, 2020; Pham & Doan, 2020; Ratnawati, 2020). Even though research proves the importance of financial inclusion for the economic progress of a country, the facts show that many small business actors experience difficulties in gaining access to formal and non-formal financial services (Bongomin et al., 2017; Brixiová et al., 2020). In Indonesia, the role of the small- and medium-sized enterprise sector has been proven to influence the country’s economy. However, data from Bank Indonesia shows that the share of the credit market for small businesses related to finance access is still low, at less than 20%. This is because many small business actors are classified as unbanked.

Data from the World Bank in 2017 shows that only around 36% or around 90 million Indonesian adults have bank accounts. This percentage is still relatively small when compared to neighboring countries, such as Malaysia with 81%, China 79%, India 53%. This low percentage is due to the presence of asymmetric information which causes financial

1

First Author. [1] PhD Student, Department of Accounting, Faculty of Economics and Business, Universitas Airlangga, Indonesia. Email:

[email protected] [2] Lecturer, Department of Accounting, Sekolah Tinggi Ilmu Ekonomi Indonesia, Indonesia.

Email: [email protected]

2

Corresponding Author. Lecturer, Department of Accounting, Faculty of Economics and Business, Universitas Airlangga, Indonesia [Postal Address: Jalan Airlangga, Surabaya, East Java, 60286, Indonesia] Email: [email protected]

3

[1] PhD Student, Department of Accounting, Faculty of Economics and Business, University Airlangga, Indonesia. Email: i.made.laut.

[email protected] [2] Lecturer, Department of Accounting, Majoring Accounting, Sekolah Tinggi Ilmu Ekonomi Bisnis dan Perbankan, Yogyakarta, Indonesia. Email: [email protected]

© Copyright: The Author(s)

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (https://creativecommons.org/licenses/by-nc/4.0/) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.