Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi:10.13106/jafeb.2021.vol8.no7.0457

Fraud Management Accounting and Organizational Value Creation:

Evidence from Listed Firms in Thailand

Kornchai PHORNLAPHATRACHAKORN

1Received: March 30, 2021 Revised: June 07, 2021 Accepted: June 17, 2021

Abstract

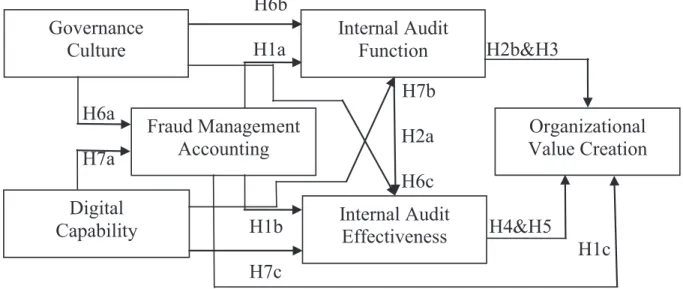

This study seeks to examine the effects of fraud management accounting on organizational value creation of listed firms in Thailand through internal audit function and internal audit effectiveness as the mediators of the study. In addition, governance culture and digital capability are hypothesized to affect fraud management accounting, internal audit function, and internal audit effectiveness. The 297 listed firms in Thailand are the samples of the study. The structural equation model is applied to test the research relationships. The results of the study indicate that, firstly, fraud management accounting has an effect on internal audit function, internal audit effectiveness, and organizational value creation. Secondly, internal audit function affects both internal audit effectiveness and organizational value creation. It also mediates the fraud management accounting-organizational value creation relationships. Thirdly, internal audit effectiveness affects organizational value creation and it mediates the fraud management accounting-organizational value creation relationships. Finally, governance culture affects fraud management accounting, internal audit function and internal audit effectiveness. Accordingly, executives can support, promote and enhance the applications of fraud management accounting in an organization, and utilize its concepts as the valuable tools in order to create best organizational practices and achieve their business goals in the current and future operations.

Keywords: Fraud Management Accounting, Internal Audit Function, Organizational Value Creation, Governance Culture, Digital Capability JEL Classification Code: M41, M42, M49

and results in financial distresses. Accordingly, firms during the COVID-19 pandemic must utilize their capabilities and strategies for creating success, survival and sustainability.

Likewise, in the COVID-19 pandemic, firms may possibly engage in unusual operations and practices through managerial misconducts and misappropriation of assets that can lead to corruption, bribery and fraud. The results of this situation have also had a strong relationship with poor performance, potential financial risk, and dissatisfied shareholders.

Fraud can be a result of the uncertain environments and unusual situations and it refers to wrongful or criminal deception intended to result in misleading financial statements that injure investors and creditors (Edge &

Falcone Sampaio, 2012). Moreover, fraud is the presentation with the intent of deceiving others, including activities, such as theft and corruption and an unlawful intention between two parties with the intent of deceiving one party (Zahari, Said, & Arshad, 2020). It is considered a cause, which can lead to the highest financial losses and internal control failures. To damp fraud in an organization, fraud management accounting is considered as an effective

1

First Author and Corresponding Author. Associate Professor, Faculty of Management Sciences and Information Technology, Nakhon Phanom University, Thailand [Postal Address: Nai Mueang, Mueang Nakhon Phanom District, Nakhon Phanom 48000, Thailand]

Email: [email protected]

© Copyright: The Author(s)

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (https://creativecommons.org/licenses/by-nc/4.0/) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.