Northeast Asia Energy Focus Northeast Asia Energy Focus

Vol.6 No.3 Autumn 2009

Inside the KEEI 2

Briefs on Northeast Asia 5

The Changing Political Economy of Foreign Investment in the

Russian Oil and Gas Industry 10

Michael Bradshaw

How can energy security be improved during oil disruption in

Northeast Asia? 18

Chul-Yong Lee

Improving of the recovery efficiency and reducing the water

flooding of oil wells 26

D. Abdeli / Z. Bekmukhametova

Chinese Natural Gas Utilization Trends 32

Anrong Gao / Tian Nan

Cooperation in the coal industry in Northeast Asia 36

Dmitry Sokolov

Nuclear energy consumption by region 42 Hydroelectricity consumption by region 42

Issue & Focus News Update

NEA Statistics

Autumn 2009/ Northeast Asia Energy Focus

Inside the KEEIThe Fourth Korea-Mongolia Joint Workshop

T

he Korea Energy Economics Institute (KEEI) and the Energy Authority (EA) of Mongolia jointly organized a workshop called the “Energy Policy/Planning Research Cooperation between Korea and Mongolia,”which was held on July 1-2, 2009, at the Lotte Hotel in Jeju Island, Korea.

The first day of the workshop comprised of four sessions, where eight speakers made presentations on the following topics:

Mongolia’s policy on new and renewable sources of energy (NRSE), uranium policy, energy-efficient heating systems, and conditions of hydropower plants as applicable to a CDM project, the possibility of Korea- Mongolia energy cooperation, the status of utilization of small-scale nuclear power plants in Korea, district heating, Korea’s NRSE policy, and so on. The presentations were interspersed with discussions and Q&A.

The first session was on energy policy dialogue; Dr. Nam-il Kim, KEEI, made a presentation on the status of the energy sector in Korea, green energy policy development, the status Korea-Mongolia energy cooperation, and the possibility of cooperation in the near future. The second session was on nuclear

power and uranium; Dr. Keun-dae Lee, KEEI, made a presentation on the status of nuclear energy in Korea, future trends, and a small- scale nuclear power reactor business involving SMART.

The third session was on district heating; Ki- eun Shim, KEEI, made a presentation on the district heating development process and the condition of Korea’s district energy supply system. The last session was on green growth;

Dr. Kyung-sool Kim, KEEI, presented some statistics, described the goal regarding and government policy for new and renewable energy in Korea, and shared success stories of Korea’s international joint ventures, including those of the DURE-Gobi project.

On the second day of the workshop, July 2, members of the KEEI and EA of Mongolia participated in an industry observation program, in which they visited and observed a thermal power plant and a wind power plant in Jeju Island.

The Seventh Meeting of the Working Group on Energy Planning and Policy

2

News Update

3

T

he seventh meeting of the Working Group on Energy Planning and Policy (WG- EPP), organized within the framework of the Intergovernmental Collaborative Mechanism on Energy Cooperation in North-East Asia, was held on June 3-4, 2009, in Bangkok, Thailand. The objectives of the meeting, which were defined beforehand, included the following: a review of the progress made on the preparation for the Joint Study on Energy Production Potential and Development Plans in North-East Asian Countries, particularly, regarding the major energy supply facilities (Bangkok, June 2, 2009); a review of the first meeting of the Ad- hoc Task Force on development of the strategy; preparation for the second North- East Asia Government-Business Dialogue;preparation for the fifth session of the Senior Officials Committee (SOC); and a review of the development of the five-year strategy for energy cooperation. The meeting was attended by representatives / experts from Mongolia, the Republic of Korea, and the Russian Federation, as well as resource persons from China and the Mekong River Commission, who shared their experiences and views on issues relevant to energy cooperation. A representative from Japan also participated as an observer. The meeting was chaired by Mr. Ryu Ji-Chul, Senior Research Fellow, Center for Energy Information and Statistics, Korea Energy Economics Institute (KEEI), and co-chaired by Mr. Igor Shcheulov, Director, International Cooperation Department, Ministry of Energy of the Russian Federation.

The agendas that were deliberated upon in the meeting are as follows:

▶Opportunities and Challenges for Energy Cooperation in North-East Asia:

Strengthening the Organizational Framework of the Collaborative Mechanism

▶Status of the Joint Study on Energy Production Potential and Development Plans in North-East Asian Countries: Major energy supply facilities

▶Preparation for the Second North-East Asia Government-Business Dialogue

▶Preparation for the Fifth Session of the SOC: Issues to be Brought to the Attention of the Senior Officials Committee

▶Five-year Strategy for Energy Cooperation in North-East Asia

▶Other matters.

Korea-China Energy Workshop

T

he Korea-China Energy Workshop was held on May 14 in Beijing, China. Dr. Ki- eun Shim and Dr. Yong-duk Pak from KEEI were the speakers at this conference.The conference comprised three sessions, namely, “Prospects of China’s domestic energy policies,” “Potentials for China-Korea energy cooperation on energy securities measure,”

and “Round-table discussion.” In the first session, Dr. Young-duk Pak, KEEI, made a presentation on the energy policy of the current Chinese 5-year plan and its prospects.

Next, Dr. Guang Yang, Energy Research Institute (ERI), National Development and

Autumn 2009/ Northeast Asia Energy Focus

Reform Commission, made a presentation on the growth in China’s energy demand and its energy security. In the second session, Dr. Ki- eun Shim, KEEI, made a presentation on the trade patterns of petroleum products between Korea and China. Further, Dr. Yousheng Zhang, ERI, made a presentation on China’s overseas energy development. In the last session, the participants were involved in a discussion on the energy policies of China, and the status and prospects of energy security. There was a strong consensus on the need for Korea and China to exchange information on their energy policies.

The Korea-Azerbaijan Commission on Economic Cooperation

T

he Korea-Azerbaijan Commission on Economic Cooperation was jointly held by Korea’s Ministry of Knowledge Economy (MKE) and Azerbaijan’s Ministry of Economic Development, on July 9, 2009. The commission was composed of 70 government and nongovernmental representatives, who discussed how the two countries can cooperate on new projects in five fields: energy resources; industry, trade, and investment;telecommunication; construction; and agriculture and forestry.

The delegation from Azerbaijan requested Korea’s contribution to Azerbaijan’s IT industry, which along with its oil industry is being promoted by the Azerbaijan government as a driving force for economic growth. Representatives from the field of energy resources organized the Third Resources Cooperation Committee and held in-depth discussions on ways to cooperate in various fields such as the development of oil fields, joint study of mineral resources, electric

power, and energy.

In May 2008, KEEI signed a memorandum of understanding (MOU) with the Azerbaijan Scientific-Research & Design-Prospecting Power Engineering Institute (AzSR&DPPEI), for research cooperation, where they agreed upon cooperation with regard to joint studies, organization of seminars, and so on.

The Ninth Meeting of the Korea- Russia Joint Committee on Energy and Natural Resources Cooperation

O

n June 30, 2009, the ninth meeting of the Korea-Russia Joint Committee on Energy and Natural Resources Cooperation was held in Seoul. The committee acknowledged the need to intensify the interaction between the Korea Energy Economics Institute and the Institute of Energy Strategy within the framework of the implementation of the MOU on Cooperation in Energy Policy Research, which was signed in September 2004. In the Moscow Summit Meeting on September 30, 2008, the KEEI and ESI signed an agreement on scientific cooperation in the area of energy policy and the sharing of expertise for 2008 to 2010.4

Autumn 2009/ Northeast Asia Energy Focus

5

Autumn 2009/ Northeast Asia Energy Focus

Briefs on Northeast AsiaChina moves toward aggressive renewable energy strategy

C

hina’s energy administration is drawing up plans to increase power generation from renewable sources to 15 percent of the nation’s total by 2020. To do so, the country will rely more on solar, wind and biomass energy with the goal of deriving more than 200 million emissions-free kilowatts.While 15 percent might not seem like a lot in California where the mandate is 33 percent of the state’s total by 2020, the figure is pretty ambitious for a country with such a massive population and higher technological hurdles.

In fact, 15 percent would be 13 times China’s current amount of energy generated by renewables. The proposal would significantly revise a current target of 60 million kilowatts by 2020.

Achieving the raised bar would require substantial financial investment by the Chinese government and private backers. Rough estimates put the amount at $658.8 billion dollars (or as high as $1.3 trillion including investments from component makers and others) - a staggering number that is closer to the U.S.’s full $787 billion stimulus package than the $60 billion going to cleantech industries.

Already, there are plans for 20 large solar power plants in Jiangsu Province, and proposals for wind power facilities to be located off the coast of Shanghai. Meeting these renewable sources halfway, the country already has a nuclear strategy in the works

that could boost that brand of energy production to 86 million kilowatts (5 percent of energy production) by 2020. On August 5, nuclear accounts for little more than 9 million kilowatts in China.

China surpassed the United States as the largest producer of greenhouse gases several years ago. Together the countries account for 40 percent of the greenhouse gas emissions in the world, according to the New York Times.

China’s goal - similar to many countries, including the U.S. - is to come up with a comprehensive and ambitious plan to present at the United Nations Climate Change Conference in Cophenhagen in December, where the global community will attempt to reach a consensus similar to the Kyoto Protocol in 1997. Heavily criticized for its pollution problems and unsustainable development policies, China is hoping to improve its profile at the meeting, where it says it will pitch a 40 percent reduction in greenhouse gas emissions for the whole world by 2020.

Re-negotiation of Oyu Tolgoi continues

O

n July 28, re-negotiation between Government of Mongolia and Ivanhoe Mines on Oyu Tolgoi deposit was launched.On July 29, the negotiation continued all day.

Bayartsogt Sangajav, Minister of Finance and Zorigt Dashdorj, Minister of Minerals and Gansukh Luumed, Minister of Environment and state secretaries of the ministries and officials, lawyers are representing Mongolian Government.

The above Ministers are authorized by the

6

Autumn 2009/ Northeast Asia Energy Focus

Cabinet to initiate the Oyu Tolgoi Investment Agreement once it is concluded.

For Ivanhoe Mines, Sam Riggal, team led by Commerce Director and John Fonioni, Vice President in charge of Legal Issues are participating in the negotiation.

Gazprom Will Ship Gas to Asia in Bid to Curb Reliance on Europe

O

AO Gazprom, the world’s biggest natural-gas producer, plans to start piping East Siberian gas to Asia, where an increase in demand over the next 20 years may outpace growth in its traditional European markets.Gazprom will send surplus gas east from the Yakutia fields, Deputy Chief Executive Officer Alexander Ananenkov said at a ceremony in the eastern town of Khabarovsk, as work began on a new pipeline to the Pacific Ocean.

A boom in Asian demand may open export opportunities as Gazprom taps new Siberian fields. The Moscow-based company, which in 2008 sent all its exports west, entered the Asian market this year by shipping liquefied gas from its Sakhalin Island development. It’s seeking to add customers in the region after pricing disputes with Ukraine disrupted shipments to Europe twice since 2006.

“Gazprom is targeting Southeast Asia because it is a logical, or natural, market” for gas from Yakutia, Mikhail Korchemkin, executive director at Pennsylvania-based consultants East European Gas Analysis, said in an e- mailed response to questions on Aug. 2. “It is a big growing market.”

Demand for gas in Asia will rise by an average

3.6 percent a year through 2030 as economic growth boosts the use of fuels, according to the International Energy Agency. While consumption has been eroded this year by the global recession, the region’s gross domestic product is set to expand by an average 4 percent annually over the next 20 years, Exxon Mobil Corp. data show.

EU Gas Use

Demand in Europe will advance at an average annual rate of 1 percent through 2030, according to the Paris-based IEA, which advises 28 industrialized countries on energy policy.

While Gazprom may benefit from increased demand in Asia, the company will need to contend with lower prices in the region.

European gas supply contracts are linked to oil with a time lag of six to nine months, meaning the 2010 price will reflect crude’s 60 percent jump this year. By contrast, Asian prices probably won’t be pegged to oil costs, Korchemkin said.

China, Asia Pacific’s fastest-growing gas market, caps prices for the fuel. The country has kept tariffs lower than international market rates to promote the use of gas over coal, according to a June report from the IEA.

Europe will continue to pay the highest prices, making it “the most attractive gas market in the long run,” Korchemkin said.

Gazprom may also face competition from other exporters to Asia, he said. Asian nations already purchase gas from Atlantic, Pacific and Middle Eastern suppliers, mostly in the form of liquefied natural gas, a business that Gazprom only entered this year.

7

Autumn 2009/ Northeast Asia Energy Focus

Eastern Development Plan

The Russian government has instructed Gazprom to coordinate its Eastern gas development plan, prioritizing supply to local residents isolated from the grid. Most gas from Sakhalin Island, which is only 100 miles from the northern tip of Japan, will be used domestically, meaning Gazprom will need to tap new Siberian fields for export, Deputy CEO Ananenkov said.

Gas demand in Russia’s Far East may reach 25 billion cubic meters in 2020, outstripping forecast production of 24 billion cubic meters from Gazprom’s Sakhalin-3 offshore project, according to company estimates.

Yakutia may pump more than double that amount. The area, which holds about 2 trillion cubic meters of gas, may produce as much as 53 billion cubic meters a year by 2030, Ananenkov said. That gas will feed a planned 2,700-kilometer (1,680-mile) pipe to Khabarovsk, which will be extended to the Pacific port of Vladivostok.

LNG, Compressed Gas

Gazprom is studying fuel exports from Vladivostok in the form of liquefied natural gas, which is gas that’s chilled to a liquid for transportation by tanker, or as compressed gas, Ananenkov said.

The company aims to send a third of its exports to new markets in the U.S. and Asia by 2030 after opening up fields in eastern Russia, Vitaly Karaganov, head of the Energy Ministry’s oil and gas department, said in June.

Russia has enough gas to supply Asian customers as well as European markets,

President Dmitry Medvedev said last September, adding that “without diversifying the development of the country eastward, our economy has no future.”

Gazprom accounted for 10 percent of Russian GDP last year, according to its Web site.

Sakhalin Supply

The company entered the market for liquefied natural gas in March when it started shipments to Asia from Russia’s first LNG plant on Sakhalin Island. Sakhalin Energy, led by Gazprom, has so far sent 27 tankers loaded with LNG, Galina Dubina, a company spokeswoman, said by telephone on Aug. 3.

It plans to ship about 55 tankers this year, she said.

An annual 7 billion cubic meters of Sakhalin gas will feed the first phase of Gazprom’s pipeline to the Pacific coast, Ananenkov said.

Transit capacity will later be expanded to 47.2 billion cubic meters to include a proposed link from the Yakutia fields, allowing exports to Asia-Pacific markets, he said.

Gazprom exported 158.8 billion cubic meters of gas to Europe last year.

Chinese official calls for strengthening energy cooperation

H

ead of Chinese delegation Liu Qi, who is vice head of China’s National Energy Administration, stressed at the 6th ASEAN+3 (China, Japan and South Korea) Ministers on Energy Meeting (AMEM+3) on July 29 that China will be a more integrated part of energy cooperation including the ASEAN+3 frame work to maintain international and regional8

Autumn 2009/ Northeast Asia Energy Focus

energy security.

With the theme of “Securing ASEAN’s energy future towards prosperity and sustainability ”, the 6th ASEAN+3 meeting officially kicked off in Myanmar’s second largest city of Mandalay.

“The Chinese government attaches great important to energy cooperation in the ASEAN+3 framework,” Liu said, adding that China hosted last October the 5th ASEAN+3 Natural Gas Forum and 4th ASEAN+3 Natural Gas Business Dialogue achieving positive results.

He also said that energy security and sustainable development still face challenges but ASEAN, China, Japan and South Korea have made continuous efforts to strengthen regional energy cooperation.

In the 3rd East Asia Summit of Energy Ministers’ Meeting (EAS-EMM) held here on the same day, Liu said, in the past year, the Chinese government has achieved success in promoting energy efficiency and conservation, opening energy market and developing biofuels.

“Since 2006, we have made important progresses in energy conservation through a combination of economic, legal and necessary governmental measures,” he said, adding that the energy consumption for unit GDP production is lowered nationally year by year, 1.79 percent lowered in 2006, 4.04 percent lowered in 2007, and 4.59 percent lowered in 2008.

Joint statements were issued by the 6th ASEAN+3 Ministers on Energy Meeting (AMEM+3) and the 3rd East Asia Summit of Energy Ministers’ Meeting (EAS-EMM).

Russian, Tajik Presidents Unveil Joint-Venture Power Plant

Tajik President Emomali Rahmon and his Russian counterpart Dmitry Medvedev have officially unveiled the fourth and last facility of the Sangtuda-1 Hydropower Plant, 160 kilometers south of the Tajik capital, Dushanbe.

The two leaders said the power plant is the most important project completed by the countries in the last 20 years.

The Kremlin and Russian companies invested some $500 million in Sangtuda-1 and own some 75 percent of its shares.

The main consumer of the energy from Sangtuda-1 is Tajik power company Barqi Tojik. The Russian management of the power plant has said several times in recent months that Barqi Tojik has not paid for the energy it uses and that the company’s debt is in the millions of dollars.

The Tajik side acknowledges the debt but says it cannot pay as companies and other consumers are not paying their energy bills.

Rahmon and Medvedev met privately on July

The Sangtuda-1 hydropower plant on the river Vakhsh

9

Autumn 2009/ Northeast Asia Energy Focus

30 after holding a four-way summit with the Afghan and Pakistani presidents, Hamid Karzai and Asif Ali Zardari, respectively.

One topic at the summit was the export of electricity including from Sangtuda-1 from Tajikistan to Afghanistan and Pakistan.

After the meeting, Medvedev’s spokesman Sergei Prikhodko said that Tajikistan’s explanation of a new draft law on the state language guarantees that the Russian language is not threatened. Moscow had been concerned that the language law would marginalize the Russian language.

Prikhodko also said both sides agreed to develop “equal military cooperation.” Some reports say Tajikistan wants Moscow to pay for its three military bases in Tajikistan, located in Dushanbe, Kulob, and Qurghon-Teppa.

Russian Energy Firm Presses Forward With World’’s First Floating Nuclear Power Plant

It’s one of those ideas that just sounds wrong:

a barge-like floating nuclear plant in the middle of the ocean. But despite its somewhat

unconventional approach, a Russian firm we first reported on in 2006 is forging ahead with plans to have the first model ready to begin service in 2012.

A floating nuclear plant, as opposed to one on land, has the advantage of being mobile.

It can be shuttled between coastal regions like a barge, delivering on-demand power to coastal industrial cities where it’s needed most.

And, in a country with plenty of experience with the potentially disastrous effects of a meltdown, the benefit of having the reactor at a safe distance from populated areas is considerable.

Conversely, there are concerns with how an ocean-borne plant will dispose of its dangerous nuclear waste or secure itself from a potential terrorist attack.

When we first reported on the project, availability was expected as early as 2010. The target date is now 2012, with the first operator already signed on to purchase the first plant at a price of 226.8 million euros.

Floating Nuclear Plant OPK

10

Autum 2009/ Northeast Asia Energy Focus

F

ebruary 18, 2009 the Russian President Dmitry Medvedev officially opened Russia’s first liquefied natural gas (LNG) plant built by the Sakhalin Energy Investment Company (hereafter Sakhalin Energy) at Prigorodnoye on the southern shores of Sakhalin Island, near the town of Korsakov.The final cost of the project is unknown, but it will be at least $22 billion. When fully operational, the plant will have a capacity of 9.6 million tonnes a year (13.3 bcm) and the majority of its output will be exported to nearby Japan, with South Korea and North America also being major consumers. At the Opening Ceremony, Christopher Finlayson, Chairman of the Board of Directors of Sakhalin Energy, said: ‘This achievement is a take-off point, which opens up a new era in the history of Sakhalin. This has only been made possible thanks to the cooperation between Sakhalin

Energy and its shareholders, the Russian Federal Government and the Sakhalin Oblast authorities.2

The Sakhalin II project is a major achievement, but the congratulatory remarks at the Opening Ceremony belie a difficult history, as the recent fate of the project has been synonymous, in

The Changing Political Economy of Foreign Investment in the Russian Oil and Gas Industry

Michael Bradshaw1

Professor of Human Geography University of Leicester, UK.

Issue & Focus

1 This is a condensed and updated version of Michael Bradshaw, The Kremlin, National Champions of the International Oil Companies: the political economy of the Russian Oil and Gas Industry, Geopolitics of Energy, 2009, 31 (5): 2-14.

2 ‘New Energy Source Comes Onstream at Sakhalin II’, Sakhalin Energy Website. Available at:

http://www.sakhalinenergy.com/en/media.asp?p=media_page&itmID=259. Accessed: 23 April 2009.

[Figure 1] The map of the Sakhalin Projects

11

Autum 2009/ Northeast Asia Energy Focus

the eyes of many western observers, with the rise of resource nationalism in Russia. This article explores the Kremlin’s changing attitude to the role of the international oil companies (IOCs) in the Russian oil and gas industry. It also considers the impact of the current global economic crisis on Russia and assesses how Russia’s changed economic fortunes might alter attitudes towards foreign investment.

The changing climate for foreign investment in the Russian oil and gas industry

In the early 1990s the fledgling Russian Government was keen to attract foreign investment and signed three production agreements (PSAs), two on Sakhalin and one in the Nenets region of the European North.

However, the level of investment remained modest and it was not until 2003 ─when BP formed its 50/50 joint venture with TNK and Shell announced commencement of Phase 2 of its Sakhalin II project--that billions of dollars of investment were committed. Even then, it is fair to say that given its reserve base and the desire of the IOCs to invest, the amount of foreign investment activity in Russia was disappointing. However, despite the positive rhetoric, one should not assume that the Russian Government and private Russian companies actually want to see substantial foreign involvement in the domestic oil and gas industry.

The change in attitude in Russia started in early 2004 when ExxonMobil had its licenses for Sakhalin III (Krinsky, Ayashsky and East Odoptu) revoked. It had become clear that, despite President Putin’s initial enthusiasm (in 2000 he attended a conference on Sakhalin

and stated that: ‘PSA’s are for Russia’), no more PSAs would be awarded in Russia and the project would not be developed without a PSA. Consequently, the Russian authorities may have felt that there was little to gain from having ExxonMobil and its partners sitting on the license doing nothing. ExxonMobil still contests the legality of this decision, but in late 2008 the Krinsky license was awarded to Gazprom without a tender process.

ExxonMobil’s Sakhalin I project has not been subject to the attentions of the Kremlin, for the simple reason that from the onset it had a Russian partner in the form of Rosneft and its Sakhalin affiliate Sakhalinmorneftegaz (SMNG). In the early stages of the project Rosneft and SMNG actually had a 40% share in the project, but they sold 20% to the Indian State Oil Company (ONGC) in 2003 for $1.7 billion to finance their continued involvement in the consortium. Although ExxonMobil is the operator through Exxon Neftgaz Limited, it has only ever had a 30% share of the project.

In marked contrast, until recently, the Sakhalin II project had no Russian involvement and, as a consequence of the departures of McDermott (US) and Marathon (US), Shell had ended up with a 55% share of Sakhalin Energy. Shell was only too aware that their position was becoming increasingly uncomfortable. Even the TNK-BP joint venture became problematic as the Kremlin pushed through legislation that required that Russian companies (by which they meant Gazprom or Rosneft) should have a controlling share of projects (51%+) that were deemed of strategic interest to the Russian state. New laws on the ‘Sub-Soil’ and ’Foreign Investment’ have now enshrined this view in the legislation. Furthermore, Russia’s 2003 energy strategy assigned Gazprom the role of

12

Autum 2009/ Northeast Asia Energy Focus

coordinating gas exports to Northeast Asia, describing it as the ‘single channel’ through which Russia would export gas to the region.

This posed problems for TNK-BP’s Kovyta project in East Siberia, as well as both Sakhalin projects, as they all planned to export gas without Gazprom’s involvement. That was in 2003. Since then the situation has changed dramatically, though, as we shall see, some disputes remain.3 The change in attitude towards the IOCs was a separate issue from the re-nationalization of domestic oil and gas production.4 The former was a matter of controlling rents and addressing domestic political and geopolitical concerns, what Bremmer and Johnston call ‘economic nationalism’, while the latter was more about

‘resource nationalism,’ a desire to stop foreign companies controlling strategic projects on

Russian territory.5In fact, with the benefit of hindsight, one might see the PSAs granted foreign companies and the sell-off of domestic oil production to the oligarchs as anomalous, and the recent measures a return to the status quo of state control and suspicion of foreign oil companies.6

The battle for Sakhalin II

In the summer of 2006 the growing tension between the Kremlin and the foreign oil companies came to a head over the Sakhalin II project. Given the scale of the project, the involvement of Shell and its location offshore of Sakhalin Island, it is no surprise that it had caught the attention of the global environmental movement. The environmental NGOs orchestrated a global campaign aimed

3Nina Poussenkova, ‘All Quiet on the Eastern Front…’Russian Analytical Digest, 33 (8): 13-18.

4Philip Hanson, ‘The Resistible Rise of State Control in the Russian Oil Industry,’Eurasian Geography and Economics, 2009, 50 (1): 14-27.

5Ian Bremmer and Robert Johnston, ‘The Rise and Fall of Resource Nationalism,’Survival, 51 (2): 149-158, 2009.

6I am grateful to Jonathan Stern for suggesting the need to see these issues from a Russian perspective. Western analysts are always likely to see FDI as necessary and private ownership more desirable than state control; neither view is predominant in Russia.

<Table 1> Foreign Investment in the Russian Oil and Gas Industry Y

Yeeaarr FFoorreeiiggnn IInnvveesstteerr && RRuussssiiaann PPaarrttnneerrss FFoorreeiiggnn IInnvveessttmmeenntt VVaalluuee

1995 TotalElfFina (France) Kharyaga PSA $2.5bn over 33

+Norsk Hydro (Norway) (Oil production in the Nenets years

+Lukoil (Russia) Autonomous Region)

+Nenets Oil Company (Russia)

1996 MCDermott (US) until 1997 Sakhalin 2 PSA $ 10 bn over 25

+Marathon Oil (SA) Until 2000 years (now $22 bn)

+Mitsui (Japan) +Shell (UK) 2006 *Gazprom (Russia)

1996 Shell (UK)-JV with OA NK Evikhon (Russia) now a 50% stake in Salym Petroleum Shell approved a budget of

subsidary of UK-based Sibir Energy plc. Development N.V more than $ 1 bn.

1996 ExxonMobil (USA) Sakhalin 1 PSA $ 15 bn over 33 years

+Sodeco (Japan) +Rosneft

2001*ONGC India (for $225)

1997 BP (UK) 10% stake in Sidanco $ 571mn

2003 BP (UK) 50% stake to create TNK-BP $ 6.75 bn

2004 Conoco Phillips (USA) 7.6% stake in Lukoil $ 1.9 bn

2005 8.5% stake in Lukoil na

2006 3.9% stake in Lukoil na

2005 Conoco Phillips (USA) JV with Lukoil(Russia) 30% stake in $ 529mn

Naryanmarneftegaz

13

Autum 2009/ Northeast Asia Energy Focus

at persuading the international financial institutions and commercial banks not to finance the project.7 The NGOs not only focused on the environmental impacts of the project, they also argued that the Sakhalin II PSA was not a good deal for the Russian Government.8 This was a claim that resonated in Moscow, particularly as the cost of the project started to escalate and the point at which the investors recovered their costs was pushed further back. In 2005 Shell had tried to negotiate an asset swap with Gazprom to give it a 25% share of Sakhalin II in return for a share in a West Siberian gas field, however, the deal collapsed when it was made public that the Sakhalin II project was facing massive cost overruns ─ a $10 billion project had become a $20 billion project. This was part of an industry-wide problem of cost increases, but Gazprom walked away from the deal.

In 2006, the cost increases and environmental campaign caught the attention of officials in Moscow at a time when the Kremlin was increasingly determined to reduce the control of the IOCs over projects like Sakhalin II and Kovytka. That the Sakhalin II project was nearing completion and that it had managed to sell all of its LNG into an increasingly profitable market must also have caught the Kremlin’s attention. As energy prices continued to increase, the Kremlin attacked the terms of the Sakhalin II PSA. At the G8 summit in 2006 President Putin described Sakhalin II as a ‘colonial treaty having nothing in common with the interests of the Russian Federation.’ The writing was on the wall for Shell and its partners.

In August and into September 2006, the Russian Ministry of Natural Resources took Sakhalin Energy to task over alleged breaches of legislation along the pipeline corridor. In Mid-September, the Minister of Natural Resources, Yuri Trutnev threatened to revoke the State Environmental Expertise Review approved in 2003. This would have brought the project to a standstill. In the end no such action was taken, but the NGO campaign had provided the Kremlin with the leverage necessary to renegotiate the structure of the Sakhalin II project. Throughout the autumn, the pressure mounted on Shell and Sakhalin Energy; Gazprom denied any involvement.

Finally, on December 21 2006, President Putin and the CEOs of Sakhalin Energy’s shareholders gathered in the Kremlin to announce that Gazprom would purchase a 50% plus 1 share interest in Sakhalin II for

$7.45 billion; each of the existing shareholders would decrease their share by 50%. In January 2007 the EBRD announced that it was no longer considering financing the project, but negotiations continued with other potential lenders. In April 2007 Gazprom took control of the project. In June 2008 Sakhalin Energy announced an agreement on financing with the Japan Bank for International Cooperation and a consortium of international banks, JBIC providing $3.7 billion and the banks $1.6 billion. The environmental concerns relating to onshore pipeline construction have gone away and the project has been winning prizes and accolades for its environmental performance. Most recently, Sakhalin Energy agreed to abandon planned seismic work for

7See Michael Bradshaw, The Greening of Global Project Finance: the Case of the Sakhalin II Oil and Gas Project’, The Canadian Geographer, 51, 3, 255- 279, 2007 for a full description of this campaign and the actions of the Russian Government. See also: Michael Bradshaw (2009) Editorial: The Sakhalin Saga, Energy Current, 28 January 2009. Available at: http://www.energycurrent.com/index.php?id=2&storyid=15571. Accessed 24 April 2009.

8See Ian Rutledge, The Sakhalin II PSA- A Production ‘Non-Sharing’Agreement, Sheffield Energy & Resources Information Service, 2004.

14

Autum 2009/ Northeast Asia Energy Focus

summer 2009 to avoid disturbing the feeding Grey Whales.

No sooner was the Sakhalin II dispute resolved then Gazprom turned its attentions to TNK-BP’s Kovytka project in Irkustk Oblast in East Siberia. There is not space enough here to delve into details,9but the bottom line is that BP and TNK-BP have been forced to sell their stake in the project to Gazprom; the final details have still yet to be resolved and neither party seems in a particular hurry to finalize an agreement.

Most recently, ExxonMobil has had problems in getting budget approval for the second phase of their Sakhalin I project. This is now resolved, but it has hampered the progress of the project. This phase aims to develop further offshore gas production and deliver it to market in China via the construction of a pipeline. Not surprisingly, Gazprom has a somewhat different plan for Sakhalin I as part of its grandiose ‘Eastern Programme’, wanting the additional gas production to be sold to the domestic market in the Russian Far East.

Finding additional gas is essential for the Sakhalin-Khabarovsk-Vladivostok gas pipeline project that is due to deliver gas to Vladivostok in 2011. Gazprom has offered to buy gas from the Sakhalin I project. ExxonMobil maintains that the terms of the PSA gives them the right to build an export pipeline and that selling the gas to China will attract a higher price than domestic sales, which is in the best interest of the Russian Government. As yet, no agreement has been reached, though there have been press reports that ExxonMobil has agreed to sell 20% of its gas output to Gazprom. ExxonMobil has denied this and

the negotiations are probably complicated by the fact that the Japanese and Indian partners in the project would rather see their shares as LNG. During President Obama’s recent visit to Moscow, ExxonMobil agreed to ‘ramp up’

their investment in Sakhalin 1, suggesting, perhaps, that a compromise has been reached in their negotiations with Gazprom.

Lessons from Sakhalin

The conflict over Sakhalin II confirmed a new set of rules governing foreign investment in the Russian oil and gas industry, and there are lessons to be learnt by all the parties involved.

First, despite the Kremlin’s opposition to PSAs, neither of the Sakhalin projects would have been developed without the PSAs agreed in the early 1990s. Notwithstanding their rocky ride, the PSAs have provided the investors with the security they need to go ahead with multi-billion dollar projects. This begs the question, if PSAs are not for Russia, how will the IOCs be persuaded to invest in the future?

It is unlikely that BP, ExxonMobil, or Shell would accept the kind of investment structure agreed to by Total and StatoilHydro on the Shtokhman project, where a special purpose company Shtokhman Development AG has been created for project (Gazprom owns 51%, Total 25% and StatoilHydro 24%); but Gazprom has retained 100% control over the eventual marketing of the output. Without clear rights to the reserves, Gazprom’s partners in Shtokhmam are operating more like service companies than oil majors. Total’s recent $ 900 million agreement with the private gas producer Novatek to develop the

9See Jonathan Stern and Michael Bradshaw, ‘Russian and Central Asian Gas Supply for Asia’, in Jonathan Stern, ed. Natural Gas in Asia, Oxford:

OUP/OEIS, 2008, 220-278, and Hyuan Ahn, ‘The Fate of Kovytka,’Northeast Asia Energy Focus, 2009, 6 (1): 12-19

Termokarstovoye gas field in the Yamal- Nenets region of West Siberia seems to be on the basis of the creation of a joint venture, ceated by Total acquiring 49% of the Novatek unit Terneftegaz, and the recent history of TNK-BP illustrates the dangers of such an approach (Gazprom currently own 19% of Novatek).

Second, it is the case that the involvement of the IOCs ─Shell and ExxonMobil ─in the Sakhalin projects has provided essential project management experience and expertise, capital and technology, without which the projects would not have been possible. It remains the case that neither Gazprom nor Rosneft has the capacity to develop future projects offshore of Sakhalin without IOC involvement. Equally, Gazprom may control Sakhalin Energy, but it has not yet acquired the ability to develop an LNG project. The fact that Gazprom, having initially rejected foreign involvement in Shotkhman, had to invite Total and StatoilHydro to participate reflects its lack of offshore and LNG experience. Prime Minister Putin has recently acknowledged these limitations in his overtures to Shell in relation to Gazprom’s Sakhalin III project. At a meeting with outgoing Shell CEO Jeroen van der Verr and incoming CEO Peter Voser, Prime Minister Putin said: ‘We consider it possible to continue a partnership with on other fields namely Sakhalin-3 and Sakhalin-4.’ ‘Your company’s competence and experience will be in demand in the remote and deep sea offshore area.”

Third, at one point in the not too distant past, in addition to Sakhalin I and II, there were as many as five potential development projects offshore of Sakhalin. Today, only one exploration project is active, Rosneft’s Veninsky project and that is not close to

development. Even if Gazprom and Shell reach an agreement on Sakhalin III, it will be some years before those fields produce oil and gas. The reality is that there was the potential to create a ‘conveyor belt’ of projects all benefitting from an established onshore service industry and a shared infrastructure. It is largely due to actions of the Russian Government that this oil and gas province is now subject to the classic ‘boom and bust’

cycle common to resource-based economic development. The Kremlin’s changing attitude towards foreign investment has not allowed Sakhalin to realize its full potential, which, is not in the interest of the region or Russia. The Russian Far East is one of the least economically developed regions of Russia and development of its oil and gas potential is important for its future development. This is recognised in Gazprom’s gasification programme for the region.

The impact of the global economic crisis on Russia

Initially, Prime Minister Putin was of the opinion that Russia was well positioned to weather the credit crunch and the associated global economic recession. For most seasoned Russia-watchers, this seemed overly optimistic. Just as Russia boomed in the years of high resource prices, averaging 7% per annum growth since 2000 and rebounding beyond 1990 levels of economic activity, it now faces a period of rapid decline. The initial 2009 budget was based on an oil price of $95 a barrel. In January Prime Minister Putin asked for the 2009 budget to be re-worked on the basis of oil at $41 a barrel and the rouble at 35.1 to the US dollar. This resulted in a drop in revenues from 21.2% of GDP to 16.6%,

15

Autumn 2009/ Northeast Asia Energy Focus

which, with increased expenditures, will result in a forecasted budget deficit of 7% of GDP, compared to a surplus of 4.1% in 2008.10In their latest reports, the World Bank projects a 7.9% decline in GDP and the IMF foresees a 6% decline; the latter is considered realistic by the Russian Ministry for Economic Development, which reports that the economy shrank by 9.5% in the first quarter of 2009.11 Because of its failure to diversify, Russia has been hard hit by declining demand for its exports and is fairing the worst amongst the G20 economies. But things could have been a lot worse had the Russian Government not been so prudent when times were good.

Russia still has substantial reserves, but the economy is now in rapid decline and it seems unlikely that it will recover before those reserves run out. What does this mean for the oil and gas industry and the future role of foreign investment?

The impact of the global financial crisis on Russia

’

s oil and gas sectorEven before the global financial crisis, there were signs that the Russian oil and gas sector was in trouble as production growth rates declined in 2007. The production increases of the last decade have not come from substantial investment in greenfield production; rather they are from delayed production and enhanced recovery from existing fields. Why has there been insufficient investment? There are a number of reasons, but insecure property rights and high levels of taxation are usually identified as the most likely key factors. Why

invest in costly exploration (particularly offshore) if you might not own the fields in the future? The new sub-soil law does not guarantee the holder of an exploration license the right to subsequently develop a field if it is found to be commercially viable. Even if a company were of the mind to develop a field, the current levels of tax and royalty payments are such that it is hard to recoup investment in the difficult and costly operating environments found in E Siberia and the Arctic offshore. Both Russian and foreign companies share the opinion that Sakhalin’s offshore potential cannot be developed under the current fiscal regime.

All the evidence suggests that Russia’s future oil and gas production will come from increasingly remote locations in Siberia and offshore in the Arctic and the Far East. Put simply, Russia is running out of cheap and easy oil to develop. This means the Russian oil and gas industry needs a high oil price if it is to develop its new production frontier; a sustained period of low prices will put a further damper on exploration and development activity. If developments were to proceed, the domestic industry needs access to capital and technology. It is estimated that the Shtokhman field needs an oil price of $45- 60 a barrel to be profitable and that overall Gazprom needs to invest $150 billion in total over the next 10 years. While Gazprom should have no problem developing onshore Siberian production (it has delayed the development of new fields on the Yamal Peninsula due to reduced demand) they may prove more costly and taking more time than anticipated. Both

16

Autumn 2009/ Northeast Asia Energy Focus

10The World Bank in Russia, Russian Economic Report, No. 18, March, 2009.

11The World Bank in Russia, Russian Economic Report, No 16, June 2009 and Nadia Popova, ‘Kelpach Says GDP Plunged by 9.5%’, Moscow Times, 24 April, 2009.

Gazprom and Rosneft have limited offshore experience. Yet the Russian Government has decreed that the two state champions will be responsible for the development of the Arctic offshore. However, the IOCs, as Sakhalin has demonstrated, do have the capital, experience and technology to access difficult oil and gas.12 China’s NOCs may be a source of capital (as demonstrated by the recent loans for oil deal with Rosneft and Transneft)13and a market for Russian oil and gas, but they too lack the technology and experience to open Russia’s resource frontier. Here our story turns full circle: over the past 4-5 years the Kremlin has alienated the IOCs and has now forced terms of engagement upon them that they may not find sufficiently attractive to take on the heightened country risk now associated with Russia, but, despite the current difficulties, the Kremlin is not going to return to the largess of the early 1990s any time soon.

Conclusion: caution is warranted

The recent economic boom in Russia will no doubt be seen as another missed opportunity in the country’s already chequered economic history. Russia failed to use a period of sustained growth to diversify its economy and to create a ‘constructive’ investment climate.

Instead of promoting a vibrant private oil and gas industry open to foreign investment, the Kremlin used the two state champions and access to cheap foreign credit to regain state control over a large part of the industry.

Subsequently, the state has also introduced legislation that curtails the role that IOCs can play in the future development of the oil and

gas industry, with fields of 50 bcm of gas or 70 million tons of oil being considered

‘strategic’ and requiring the approval of a special government commission if foreign companies are to be involved in their development. But the reality is that the development of new productive capacity in Russia will be costly and technologically challenging and this will require partnership with the IOCs. Clearly, the Kremlin believes that IOCs are so desperate to gain access to new reserves that the likes of Shell and BP will

‘forgive and forget’, but instead it may be a case of ‘once bitten twice shy’. Prime Minister Putin and Gazprom may consider Shell an obvious partner for Sakhalin III, but will Shell invest billions in another Sakhalin project, particularly one that will not be protected by a PSA? They may well be right, it is the case that BP, Shell and Total have all positioned themselves to be able to respond to new opportunities in Russia in the Arctic offshore and early indications are that they may be prepared to accept the new terms of engagement, but the current global economic situation demands caution. Continued economic hardship in Russia might result in a softening of the Kremlin’s attitudes towards the IOCs; one would think so if one believed all the platitudes at the ceremony on Sakhalin in February, as well as Prime Minster Putin’s recent flattery of Shell; but the reality is that nothing has really changed. Even if it does, the IOCs cannot afford to be seen to be exploiting Russia’s current economic difficulties for their own reward; the lesson from Sakhalin II is that too good a deal is never a good deal.

17

Autumn 2009/ Northeast Asia Energy Focus

12See Nina Poussenkova, ‘Gazprom and Russia’s Great Eastern Pipe-Dreams,’Russian Analytical Digest, 58 (9), 2009.

13See Stephen Blank, ‘Loans for Oil, the Russo-Chinese Deal and Its Implications,’Northeast Asian Energy Focus, 2009, 6 (2): 19-30.

18

Autum 2009/ Northeast Asia Energy Focus Introduction

H

istorically, the price increase of petroleum has been caused due to either supply disruptions or high demand in developed and developing countries. Since the mid-1970s, there have been about five significant increases in the prices of crude oil and petroleum products: the Arab oil embargo (1973-1974), the deposing of the Shah of Iran followed by the Iranian revolution (1979-1980), the first Gulf War (1990), OPEC production cuts and a resurgence in world oil demand (from early 1999 to the fall of 2000), and Hurricane Katrina (the fall of 2005).Unfortunately, elevated petroleum prices affect the balance of trade owing to the relative inelasticity of the demand for petroleum.

At first, the Strategic Petroleum Reserve (SPR) was launched to help prevent a repetition of the economic crisis caused by the Arab oil embargo. In the event of an interruption, introduction of reserved oil into the market was expected to help calm markets, mitigate sharp price spikes, and reduce the economic crisis that had accompanied the 1973 disruption. By doing so, the SPR would also buy time for the crisis to sort itself out or for

diplomacy to seek some resolution before a potentially severe oil shortage escalated the crisis beyond diplomacy. Signatories to the International Energy Agency (IEA) are committed to maintaining emergency reserves equivalent to 90 days of net imports, developing programs for demand restraint in the event of emergencies, and agreeing to participate in the allocation of oil deliveries among the signatory nations to balance a shortage among IEA members. An important question to ask at this point is whether these signatories and the measures taken by them are enough to improve energy security during oil disruption.

Trend and Perspective of World Oil Market

Crude oil prices had briefly exceeded $145 per barrel by mid-July 2008. Oil prices had risen by mid-2008 in the absence of the normal association with the concept of disruption or shortage. There are several factors involved in the increase of prices; it is difficult to estimate their extent of involvement. Of these, the main factors are the existence of little or no spare oil production capacity worldwide and a general inelasticity in demand for oil products despite high prices. Price has also proven sensitive to international tensions, the value of the U.S. dollar, and even the appearance of storms that could develop into hurricanes.

Even though crude oil prices declined to $40 per barrel by the end of December 2008 and were maintained at $60 per barrel in July 2009, it seems that oil prices may reach $100 per

How can energy security be improved during oil disruption in Northeast Asia?

Chul-Yong Lee

Research Fellow

Korea Energy Economics Institute

19

Autum 2009/ Northeast Asia Energy Focus

barrel in the near future (Figure 11).

Global Oil Demand

IEA reported that the world oil demand in 2010 is expected to rebound by 1.7% or 1.4 million b/d every year to 85.2 million b/d even though the demand in 2009 is expected to decrease by -2.9% or -2.5 million b/d compared to the demand in 2008. A strong rebound such as this is largely led by non- OECD countries. China, the Middle East, and, to a lesser extent, Latin America will play a prominent role in this demand rebound. In particular, China’s demand in terms of refinery output, net oil product imports, adjusted for fuel oil, direct crude burning, and stock changes apparently jumped by 9.5% every year in May 2009. As much as the Chinese oil demand rebound may suggest an ongoing economic revival, increasing air travel and buoyant vehicle sales, it was also undoubtedly related to reserving petroleum ahead of the expected retail price increases (IEA, July 2009).

Similar to the Chinese case, countries with oil such as Brazil, Russia, and Arab are likely to have a high oil demand as their economies are becoming stable due to oil price increase.

The price elasticity of demand is now smaller than what it was in 1980, which means that the percentage change in quantity demanded is smaller in the fixed percentage change in oil price. Hughes, Knittel, and Sperling (2008) estimated that the short-run gasoline demand elasticity was in the range of -0.21 to -0.34 between 1975 and 1980 and only in the range of -0.034 to -0.077 between 2001 and 2006. One of the reasons for this may have been the falling share of oil costs in the total expenditures, which means that people continued to buy oil, despite the high price, because they could afford to ignore the price changes more easily in 2006 than they could in 1980. The growth in petroleum demand is a new emerging trend, aggravated by gasoline subsidies in many of the oil producing countries. The Middle East saw a growth of about 17% between 2003 and 2006. The rise in petroleum demand is associated with rapidly growing countries, with China alone accounting for 33%. China’s demand grew at a phenomenal 7.2% annual logarithmic rate between 1991 and 2006. During 2006, China used about two barrels of oil per person. For comparison, Mexico used 6.6 barrels of oil per person. Even if the Chinese oil consumption increased by three times, it would still be lesser than the current oil consumption in Mexico.

The U.S. used almost 25 barrels per person. In 2006, there were 3.3 passenger vehicles per 100 Chinese residents compared to 77 in the U.S. (Auffhammer and Carson, 2008). These facts can help us predict the future oil consumption in China.

Global Oil Supply

The oil supply in 2009 is expected to rise by 190 kb/d in non-OPEC countries on the basis of output that has been consistently stronger

1 World oil price projections were estimated using the Bayesian oil forecasting model in Korea Energy Economics Institute.

[Figure 1] World oil prices, 1980-2020 (Dubai, Nominal value)

20

Autum 2009/ Northeast Asia Energy Focus

than the expected Russian output in the first half of the year, recovery at Azerbaijan’s ACG field, and relatively robust U.S. and North Sea production (IEA, July 2009). The non-OPEC supply is estimated to rise by a further 410 kb/d to 51.2 mb/d in 2010, with a strong growth in Azerbaijan, Brazil, global biofuels, the U.S. Gulf of Mexico, and Canadian oil sands. However, the UK, Norway, and Mexico are expected to witness a steadily declining output. In the long run, as more oil is extracted, less will remain in the original deposit, making it increasingly difficult to continue extracting oil at the same rate.

Clearly, a decrease has now been observed in the number of oil producing areas. Oil production in the UK and Norway has been declining by 7% every year since 2002.

Mexico’s Cantarell complex, second only to Saudi Arabia’s Ghawar in terms of its contribution to recent production levels, is sharply decreasing. Although China was once a net petroleum exporter, oil production is currently decreasing in three of its largest fields (Kambara and Howe, 2007) despite new Chinese fields being sufficient so far to allow the total Chinese production to modestly increase regardless of the maturity of its major producing areas.

Apart from geological considerations, political instabilities and mismanagement have also contributed to declining oil production in countries such as Iraq, Nigeria, Iran, Venezuela, Mexico, and Russia. This interaction between such above-ground risks and resource depletion exists because it is not feasible to increase production at the historically stable regions. A 2008 study by Cambridge Energy Research Associates estimated the decline rate of global production to be 4.5% (Wall Street Journal, January 2008).

IEA estimated a decline rate of more than 3.7%

(IEA, 2007). Assuming a decline rate of 4%, global production would decline by 3.4 mb/d each year in the absence of new projects.

Unfortunately, the global investment for

exploration and production (E&P) of petroleum has declined since 2008 (Table 1).

According to IEA, investments in petroleum up-stream have been delayed or canceled by

$170 billion.

We have also experienced some cases of oil supply disruptions. Table 2 indicates the types of oil market disruptions witnessed from 1950 to 2003. Supply disruptions often lead to global oil price shocks. In addition, oil price shocks can cause reduced output, other economic dislocations, and increased cost of oil imports.

Given the increasing demand and decreasing growth rate of production, it is important to take some measures for our future. The next section sheds some light in this regard.

Strategic Petroleum Reserve

The strong growth in demand and the failure

<Table 1> Global investment for exploration and production of petroleum

(Unit: Billion $)

Source: Weekly Petroleum Argus (January 2009) C

Coouunnttrryy 22000088 22000099 %% cchhaannggee

North America 13.50 10.06 -25%

Non-North America 31.86 29.96 -6%

World 45.36 40.02 -12%

<Table 2> Types of oil market disruptions from 1950 to 2003

Accident 5 5.2 1.1

International

Political Struggle 9 6.5 2.3

International Embargos/

Economic Disputes 4-6** 11.0 (6.1*) 6.2

Wars in the Middle East 4-7**

Total/Average 24 8.1 (6.0*) 3.7

Note: * Excluding the 44-month Iranian Oilfield Nationalization

** Some events are difficult to classify Source: Event listing from the U.S. EIA

TTyyppee NNuummbbeerr DDuurraattiioonn ((mmoonntthhss)) SSiizzee ((%% wwoorrlldd ssuuppppllyy))

21

Autum 2009/ Northeast Asia Energy Focus

of global production increase threaten our economy and security in the future. The SPR can be one of the solutions to reduce the adverse economic impact of a major petroleum supply interruption and carry out obligations under the International Energy Program. The SPR is the largest emergency crude oil reserve in the world and is highly visible when oil prices rise or when global conflicts cause a potential oil supply disruption. The SPR is one nation’s energy insurance against disruptions to the world’s flow of crude oil.

It is important for IEA member countries to ensure that the SPR meets the international standards for emergency oil reserves, i.e., at least 90 days of net oil imports for the previous year. However, this standard involves many controversies because each country faces different situations in terms of oil reserves, consumption, dependence on imports, and so on. Table 3 shows the dependence on imports and oil from exploration in some countries, which may have an impact on the oil storage level.

We need to pay attention to South Korea and Japan, which are the only Northeast Asian countries that are members of IEA. The common characteristics between them are

higher dependence on imports - most of them are from the Middle East - and lower exploration rate than the U.S., Germany, and France. It means that these countries have very poor energy security. The next section shows the SPR status of countries such as South Korea, Japan, Russia, Taiwan, and China.

SPR in Northeast Asia and the U.S.

Table 4 indicates the stock level, including the

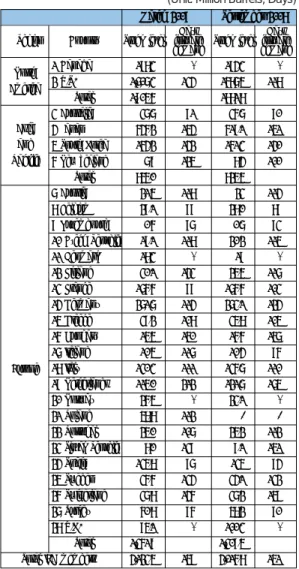

Note: 1) Source: BP Statistical Review of World Energy (2008) (June 2008) 2) 2006 Dependence on the Middle East (2007 values in South Korea) 3) Source: Petroleum Intelligence Weekly, December 2007 4) Source: Japanese Oil Development, April 2007

<Table 3> Dependence on imports and exploration rate (2007) (Unit: 1,000 b/d) SSoouutthh KKoorreeaa UU..SS.. JJaappaann GGeerrmmaannyy FFrraannccee Consumption (a) 2,371 20,698 5,051 2,393 1,919 Oil imports (b) 2,371 13,819 5,051 2,393 1,919 Dependence on

imports (c = b/a) 100% 66.8% 100% 100% 100%

Dependence on

the Middle East (d)2) 81.7% 22.0% 89.2% 10.5% 26.4%

Oil from exploration (e)3) 100 6,879 5964) 244 1,542 Ratio(g = e/b) 4.2% 49.8% 11.8% 10.2% 80.4%

Note: * Net exporting countries Source: IEA Oil Market Report (2009)

<Table 4> Total stocks on land in IEA member countries (Unit: Million Barrels, Days)

1 Canada 198.3 * 194.3 *

2 U.S. 1,707.3 134 1687.5 118

Total 1,905.6 1881.8

3 Australia 37.7 91 36.7 90

4 Japan 646.2 154 619.1 151

5 South Korea 164.2 142 161.3 140

6 New Zealand 7.9 125 8.4 100

Total 856.0 825.5

7 Austria 21.5 118 23 114

8 Belgium 29.1 99 28.0 89

9 Luxembourg 0.6 97 0.7 93

10 Czech Republic 19.1 118 20.2 115

11 Denmark 18.3 * 19 *

12 Finland 30.1 143 25.5 117

13 France 176.6 99 176.6 103

14 Germany 271.7 114 273.1 124

15 Greece 39.2 108 35.8 105

16 Hungary 15.5 150 16.6 157

17 Ireland 10.5 117 10.4 96

18 Italy 130.3 111 136.7 110

19 Netherlands 115.0 212 121.7 175

20 Norway 26.5 * 23.1 *

21 Poland 58.8 112 - -

22 Portugal 25.0 107 25.2 112

23 Slovak Republic 8.0 139 9.1 151

24 Spain 135.8 97 135 94

25 Sweden 36.6 134 34.1 132

26 Switzerland 37.8 146 37.2 159

27 Turkey 60.8 96 58.2 90

28 U.K. 95.1 * 100.3 *

Total 1,361.9 1,309.5

Total IEA members 4,123.5 159 4,016.8 151 M

Maarrcchh 22000099 SSeepptteemmbbeerr 22000088 Region Country Stock level Days

Stock level Days

forward forward

demand demand

North America

Asia and Pacific

Europe

22

Autum 2007/ Northeast Asia Energy Focus

SPR and industry stock, and days of net import cover in IEA membership countries.

The SPRs of the U.S., South Korea, Japan, and Germany amount to approximately 134, 142, 154, and 114 days of net import cover, respectively, all of which are over 90 days of IEA standard.

As of now, the combined government and private-sector crude and products stocks of South Korea are sufficient to cover more than 140 days of net imports─higher than the IEA’s 90-day requirement for it members. However, the SPR of South Korea amounts to only 76 days of actual consumption, which is too low.

Because Naphtha, the single biggest component in South Korea’s oil demand, is a feedstock rather than an end-consumer fuel, it is not included in the country’s strategic reserve planning. Considering the dependency on imports and the oil from exploration in South Korea, the SPR should definitely be more.

South Korea’s plans for increasing its SPR are constantly being postponed due to unexpected factors. In December 2006, the Korea National Oil Corp. (KNOC) was assigned the task of boosting the total strategic crude and product stocks from 118 million barrels to 141 million barrels by 2010. However, since then, oil prices have risen and the Korean won has weakened.

As a result, the Korean government and KNOC changed the original plan of the feasibility of 2010 to 2013. Moreover, the plan with 146 million barrels of SPR capacity was delayed from 2009 to 2011. The current SPR capacity of South Korea is 139.5 million barrels.

Japan started to reserve strategic oil since 1978 with a goal of 189 million barrel. Later, this goal was adjusted to 315 million barrels and achieved in February 1998. Following Hurricane Katrina in 2005, the Japanese government realized that the SPR was the best way to increase energy security.

At present, Japan holds a whopping 321 million barrels of crude in its SPR, which is equivalent to 101 days of forward demand

cover, with private-sector crude and product stocks of 250 million barrels providing an additional 81 days of cover. Japan is also planning to add products, particularly kerosene, to its SPR after the U.S. hurricane- related supply disruption in 2005. However, the goal of private-sector crude stocks was moved from 70 days of demand cover to 60- 65 days. The Japanese SPR is run by Japan Oil, Gas and Metals National Cooperation.

The Chinese government has been very active in buying crude, particularly from West Africa, to build its SPR and plans to have 90 days of net imports, in keeping with the IEA standards, in 15 years’ time. As of now, China has successfully executed the first plan of constructing four storage facilities; the Chinese plan for the SPR involves three stages that will be completed over a period of 15 years.

Recently, China increased its stockpiling efforts as oil prices eased in the fourth quarter of 2008.

Customs data show that imports from Saudi Arabia were increased. Saudi imports jumped by 61% year-on-year in the fourth quarter 2008 to 889,000 barrels per day, reaching 938,000 b/d in November (Petroleum Intelligence Weekly, May 9 2009, p.3). It is believed to be the first 100 million barrel phase of the country’s strategic reserve, which provides 28 days of import cover and which has now reached its limits. According to Dr. Kang Wu of the Honolulu-based East-West Center Thinktank, the second phase of the strategic reserve will be more flexible than the first one in terms of location, products stored, and operation. Plans for the second phase include 280 million barrels across eight sites by 2011.

While coastal locations were selected for the first phase, sites for the second phase could be places far from major consumption centers in western Xinjiang province and Gansu in central China, which would facilitate the storage of surplus domestic crude from Xinjiang’s Tarim Basin fields. Oil products in addition to crude oil could be stored for the second phase, and the bigger business such

23

Autumn 2009/ Northeast Asia Energy Focus

as leasing spare storage capacity in state firms Sinopec and PetroChina may be operated.

Further, the Chinese government is considering the possibility of floating storage and leasing from private oil firms.

Even in Russia, the Ministry of Energy (ME) is involved in the selection of oil deposits to create a reserve fund, which is essentially blocks with extractable reserves of 30 million tons of oil. It means preserving over ten deposits in the undistributed fund. By doing so, the Russian government is making efforts to ensure the future Russian needs for SPR. In Russia, the concept of strategic reserve fund has only recently appeared, and amendments to the law “About Subsoil” were made last April. The legal intent is to protect the national interests of Russia and form a predictable and favorable business climate for foreign investors. The future of this fund will depend, first of all, on the m