http://dx.doi.org/10.3938/NPSM.67.548

Text Network Analysis of Financial Information for Consumer Decision-Making

Kyungyoung Ohk

Department of Consumer Economics, Sookmyung Women’s University, Seoul 04310, Korea

Miyea Kim

∗Research Institute of ICT Convergence, Sookmyung Women’s University, Seoul 04310, Korea

Kayeong Kim

Department of Consumer Economics, Sookmyung Women’s University, Seoul 04310, Korea (Received 10 January 2017 : revised 16 March 2017 : accepted 16 March 2017)

Recently, insufficient information has led to consumer health-insurance duplication. This study determines which financial information is essential to consumer decision-making. Consumers’ health- insurance consultations were analyzed in three stages of decision-making (pre-enrollment, enroll- ment, and post-enrollment) through text mining and text network analysis. Higher frequency words were identified for each of the three stages. For example, these included “inquiry” and “fee-for- service health” at pre-enrollment; “indemnity health insurance” and “insurance agent” at the time of enrollment; and “claim,” “compensation,” and “benefits” after enrollment. Also, centrality of the text network analysis identified the terms that were located centrally on a graph in each of the three stages. Results confirmed that different information is required for each decision-making stages.

PACS numbers: 06.30.-k

Keywords: Text mining, Text network analysis, Consumer decision-making, Financial information, Indemnity health insurance

I. INTRODUCTION

Recently, up to 1.74 million consumers experienced fi- nancial loss through double insurance. In order to pro- tect consumer rights, the Financial Services Commission (FSC) is considering adopting mandatory requirements to enable consumers to confirm whether their insurances overlapped. Indemnity health insurance cannot be ap- plied multiple times, which could be problematic for con- sumers that are unaware of this fact. It is essential to give consumers accurate information about financial services, as they could make a loss due to a lack of information.

In order to understand the essential information re- quirements in consumer decision-making when choos- ing financial services, this study conducts text mining

∗E-mail:[email protected]

and text network analysis of indemnity health insurance.

This research obtained data from consultations toward indemnity health insurance from 1372 Consumer Coun- seling Centers. For the purpose of data processing, we divided the consumer decision-making process into three steps, and analyzed consumer issues in each step using text mining. The steps are as follows—step 1: problem recognition and information search (at pre-enrollment);

step 2: purchase (at the time of enrollment); and step 3:

post-purchase behavior (after enrollment).

Consumers’ recognition of various problems informs their future decision-making. Consumer decision-making is a series of processes comprised of problem recognition, information search, alternative evaluation, purchase, and post-purchase behavior [1]. Problem recognition is re- quired to reconcile the difference between the actual and the desired states, starting with a question about what

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (http://creativecommons.org/licenses/by-nc/3.0) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.

to buy [2]. Through problem recognition, a consumer explores information by doing an internal search using information in memory, or an external search to acquire new information. Then, after the information obtained in the information search is evaluated according to evalua- tion criteria such as the purchasing motive or situation, the decision is implemented through the purchase and post-purchase processes.

The financial services used by a consumer can also lead to consumer satisfaction or dissatisfaction through the decision-making series mentioned above [3]. A con- sumer who uses indemnity health insurance may have problems at each level of the process [4,5]. In this study, we divide consumer decision-making into three stages:

at pre-enrollment, at the time of enrollment, and after enrollment, and provide implications by identifying con- sumer issues raised at each stage. In order to achieve the goals of our research, we composed three research questions as follows. We analyzed the contents of consul- tations about indemnity health insurance through text mining, and analyzed keywords of frequently mentioned words at each stage according to the consumer decision- making process of consultation (research question 1). We then analyzed the linkage between the consultation data through support and confidence analysis based on the extracted keywords (research question 2). Finally, key- word network analysis was performed by nodes and links, which refer to extracted words and the relativity between words (research question 3).

II. RESEARCH METHODOLOGY

1. Data

Based on previous studies, our research used 436 cases of counseling data about indemnity health in- surance—which is a private insurance—collected among consumer counseling and damage relief data from 1372 Consumer Counseling Centers. The 436 counseling case results were classified into three levels according to con- sumer decision-making, and analyzed by using data from 54 cases in pre-enrollment, 79 cases at the time of enroll- ment, and 303 cases after enrollment.

2. Methodology

1) Text mining

Text mining is an information technology that finds meaningful information and knowledge from formal or informal text data based on natural language processing technology [6]. Using text-mining technology, researchers can extract meaningful information from large amounts of data, such as consumer and corporate data, and under- stand their connectivity to other information [6,7]. The importance of text mining is emphasized due to its po- tential as a strategy to understand the implicit meaning of text based on simple data analysis.

Text mining has many advantages, in that it can ex- tract concepts from text, comprehend the relation with other concepts, and visualize relationships between con- cepts. Since former contents analysis only depended on random items set by researchers, it was impossible to an- alyze the board parts; its reliance on coders made it diffi- cult to obtain external validity. In contrast, text-mining analysis can be applied to various researches, including big data [8] analysis social network analysis methods (which have been frequently conducted in recent stud- ies), and analysis using consumer reviews [9]. Therefore, it is not subject to the limits of conventional content analysis.

2) Text network analysis

Text network analysis is a method that analyzes text (that is, qualitative data consisting of language). It is a method used to interpret the relationship among words, between words and extracted text, or among concepts (which is collection of one or more words), and then to determine the network. Simultaneous existence of words or concepts in a text- based paragraph or sentence could imply that they establish a close conceptual connection to each other. Text network analysis is useful in various aspects [10], since it can derive meaningful interpreta- tions by understanding the relationships between words and concepts.

In conclusion, the purpose of text mining is to ex- tract information of interest from contents, and to find

Table 1. Frequency analysis by consumer decision-making stage.

no. At the pre-enrollment At the time of enrollment After enrollment

keyword frequency keyword frequency keyword frequency

1 Inquiry 21 Indemnity health

39 Claim 114

insurance 2 Fee-for-service

14 Insurance agent 34 Indemnity health

health insurance 108

3 Indemnity health

13 Application 29 Compensation 106

insurance

4 Application 11 Insurer 22 Benefits 105

5 Insurer 10 Fee-for-service

21 Fee-for-service

health health 95

6 Compensation 9 Compensation 20 Application 91

7 Denial 7 Renewal 18 Inquiry 81

8 Insurance agent 7 Explanation 18 Payment 77

9 Requirement 7 Inquiry 17 Hospital 74

10 Termination 7 Fact 17 Treatment 72

11 Insurance premium 6 Requirement 16 Operation 62

12 Insurance product 6 Termination 16 Requirement 62

13 Possible 5 Notice 15 Insurer 57

14 Hospital 5 I 15 Hospitalization 56

15 Fact 5 Insurance product 15 Insurance premium 52

summarized information through meaningful concepts.

Therefore, in this research, we use text-mining analysis to identify major issues pertaining to consumers’ view- points by utilizing cases of consumer counseling about especially indemnity health insurance in financial ser- vices, classified according to consumer decision-making stage.

III. RESEARCH RESULTS

1. Main keywords by consumer decision-making stage

We conducted a text frequency analysis to identify overall consumer issues that occurred at different con- sumer decision-making stages. High frequency nouns differed according to consumer decision-making stage.

The keywords that marked high usage frequency in the stage of pre-enrollment were: “Inquiry,” “Fee-for- service health,” “Indemnity health insurance,” and

“Application.” At the time of enrollment, the fre- quently used words were “Indemnity health insur- ance,” “Insurance agent,” “Application,” and “Insurer.”

Finally, after enrollment, the following words were used frequently: “Claim,” “Indemnity health insur- ance,” “Compensation,” “Benefits,” and “Fee-for-service health.” The results of the frequency analysis are pre- sented in Table 1, that is, the consumer issues in con- sumer counselling results about indemnity health insur- ance that occur with high frequency, divided by three levels of consumer decision-making.

2. Support and confidence of the keywords

In research question 2, we conducted an association analysis to extract the support and confidence of words in accordance with the keywords of consumer inquiry about indemnity health insurance by each level. Based on the contents of consumer inquiries by the three stages used above, we set up support; this implies a proba- bility of simultaneous discovery of 0.03; we then con- ducted association analysis. At the pre-enrollment stage, the probability of referring to “insurer,” “inquiry,” and

“Fee-for-service health,” “application” respectively was 0.0339. At the time of enrollment, the probability that

“insurance agent” will be mentioned was 0.0904 in cases

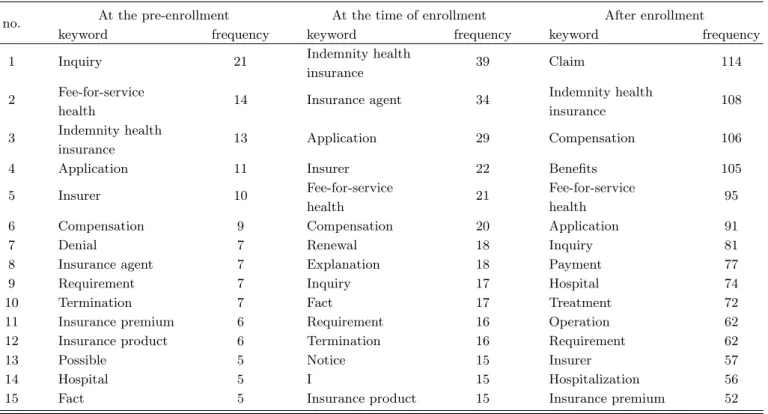

Fig. 1. (Color online) The result of the text network analysis at the pre-enrollment.

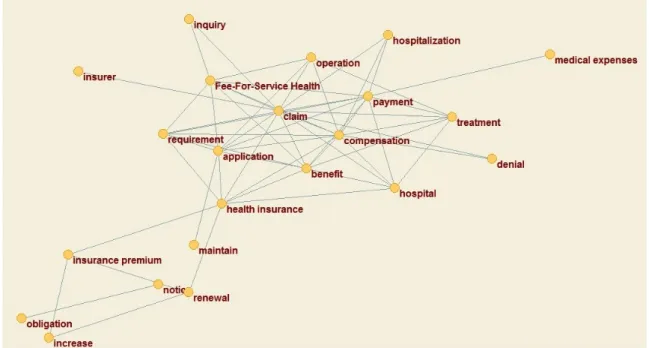

Fig. 2. (Color online) The result of the text network analysis at the time of enrollment.

where “indemnity health insurance” was mentioned. Af- ter enrollment, the probability of mentioning “benefits”

and “claim” simultaneously was 0.1166. In this way, we could confirm through association analysis that the con- sultation keywords of consumers are different in each stage.

Confidence refers to the probability that a conse-

quent word is mentioned after referring to an antecedent word. At pre-enrollment, the result shows that the probability that “indemnity health insurance” is men- tioned as consequent word of “home shopping,” and that “requirement” appeared as consequent subject to

“information” is 0.6667. At the time of enrollment, the probability mentioned “violation” or “notice” after refer-

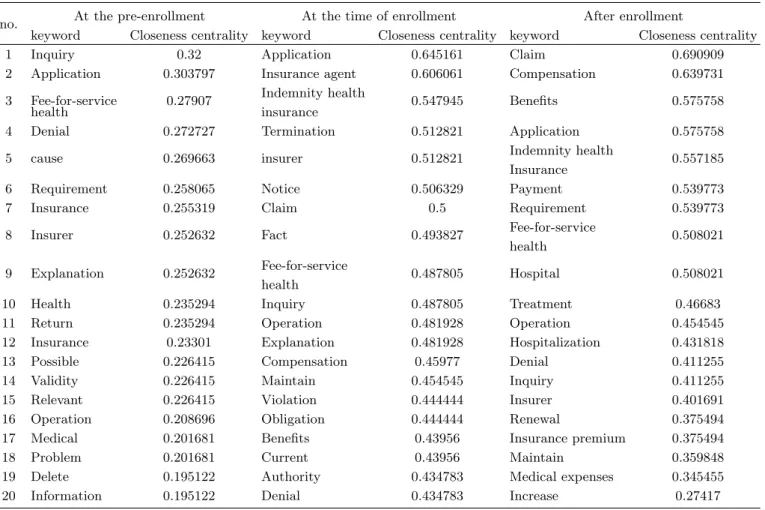

Fig. 3. (Color online) The result of the text network analysis after enrollment.

ring to “obligation” is 1.0000. After enrollment, the con- fidence value of the antecedent words “obligation” and consequent words “notice” is 0.9048. Further, the prob- ability of mentioning “renewal” or “premium” following

“increase” is 0.7436.

3. Text network analysis based on the consulta- tion keyword

In research question 3, we analyzed the network based on consultation keywords about indemnity health in- surance, and results are shown in the figures below.

First, a variety of keywords is evenly associated with

“inquiry” at the pre-enrollment stage (Fig. 1). Second, most of the keywords are directly connected to “notice”,

“insurance agent” and “application” at the time of en- rollment stage (Fig. 2). Finally, many keywords are as- sociated with “claim” and “compensation” at the post enrollment stage (Fig. 3).

Closeness centrality measures how many steps on av- erage it takes for an individual to reach everyone else in the network. In other words, individuals with high close- ness centrality can reach other individual in the network more quickly. Closeness centrality can be determined by measuring the sum of the distance between two individ- uals in nodes [11,12].

If we consider the closeness centrality of the network of consumer decision-making at level 1, “inquiry” has the highest centrality of 0.32 at pre-enrollment. The second one is “application” with a value of 0.303, and the next is

“fee-for-service health” with a centrality of 0.279. At the first stage of insurance information searching, it seems that the words above are derived from situations in which consumers make inquiries about insurance enrollment.

At the time of enrollment, “application” has the high- est value, 0.645, followed by “insurance agent” with 0.606, “indemnity health insurance” with 0.547, and

“insurer” and “termination” at 0.512. In the second stage of insurance enrollment, it is possible to see the impor- tant role of the insurance agent in the process of enroll- ment. In particular, it can be confirmed that there are many problems such as breach of duty of disclosure due to insufficient information notification by the insurance agent at the time of enrollment.

After enrollment (that is, the last level), “claim” has the highest value at 0.690, followed by “compensation”

at 0.639, “benefits” and “application” at 0.575 (Table 2). At the third stage of post-enrollment, two key words were drawn from consultation, including claims for com- pensation and benefits for hospitalization, surgery, and treatment, and complaints from consumers who have not been compensated properly for various problems.

Table 2. The closeness centrality of the network by consumer decision-making stage.

no. At the pre-enrollment At the time of enrollment After enrollment

keyword Closeness centrality keyword Closeness centrality keyword Closeness centrality

1 Inquiry 0.32 Application 0.645161 Claim 0.690909

2 Application 0.303797 Insurance agent 0.606061 Compensation 0.639731

3 Fee-for-service 0.27907 Indemnity health

0.547945 Benefits 0.575758

health insurance

4 Denial 0.272727 Termination 0.512821 Application 0.575758

5 cause 0.269663 insurer 0.512821 Indemnity health

0.557185 Insurance

6 Requirement 0.258065 Notice 0.506329 Payment 0.539773

7 Insurance 0.255319 Claim 0.5 Requirement 0.539773

8 Insurer 0.252632 Fact 0.493827 Fee-for-service

0.508021 health

9 Explanation 0.252632 Fee-for-service

0.487805 Hospital 0.508021

health

10 Health 0.235294 Inquiry 0.487805 Treatment 0.46683

11 Return 0.235294 Operation 0.481928 Operation 0.454545

12 Insurance 0.23301 Explanation 0.481928 Hospitalization 0.431818

13 Possible 0.226415 Compensation 0.45977 Denial 0.411255

14 Validity 0.226415 Maintain 0.454545 Inquiry 0.411255

15 Relevant 0.226415 Violation 0.444444 Insurer 0.401691

16 Operation 0.208696 Obligation 0.444444 Renewal 0.375494

17 Medical 0.201681 Benefits 0.43956 Insurance premium 0.375494

18 Problem 0.201681 Current 0.43956 Maintain 0.359848

19 Delete 0.195122 Authority 0.434783 Medical expenses 0.345455

20 Information 0.195122 Denial 0.434783 Increase 0.27417

Through this, it can be confirmed once again that the necessary information and inconveniences of the con- sumer are different depending on when the consumer makes decisions about insurance services. This result shows that information such as duty of disclosure or dou- ble enrollment of coverage is indispensable and must be delivered at the initiation stage.

IV. CONCLUSION

Recently, as financial complaints have increased, the Financial Supervisory Service (FSS) created standards and evaluated them to reduce the complaints of finan- cial institutions. Since indemnity health insurance is the most commonly used service, it is essential to provide ac- curate information when consumers need financial infor- mation to increase service convenience as well as service maintenance.

The aim of our research was to understand what infor- mation is required by consumers at each decision-making stage in inquiries pertaining to the inconvenience of us- ing indemnity health insurance. We analyzed the data of 1372 consultations by text mining. Through this study, it was confirmed that the required information differs by consumer decision-making stage. In addition, it is ex- pected that firms will be able to present consumers with accurate required financial information according to the consumer decision-making stage.

REFERENCES

[1] H. S. Lee, K. H. Ahn and Y. W. Ha, Consumer Be- havior, 6th ed. (JypHyunJae Publishing Co., Seoul, 2015).

[2] J. F. Engel and R. D. Blackwell, Consumer Behav- ior, 4th ed. (Dryden Press, Chicago, 1995).

[3] R. L. Oliver, J. of Marketing Research 17, 460 (1980).

[4] B. Howcroft, P. Hewer and R. Hamilton, Service Industries J. 23, 63 (2003).

[5] N. J. Black, A. Lockett, C. Ennew, H. Winklhofer and S. McKechnie, Intl. J. of Bank Marketing 20, 161 (2002).

[6] W. Fan, L. Wallace, S. Rich and Z. Zhang, Com- munications of the ACM 49, 76 (2006).

[7] J. M. Lee and J. Y. Rha, Consumer Studies 26, 93 (2015).

[8] J. Diesner and K. M. Carley, Revealing Social Struc- ture from Texts: Meta-matrix Text Analysis as a Novel Method for Network Text Analysis, Causal

Mapping for Information Systems and Technology Research: Approaches, Advances, and Illustrations, edited by V. K. Narayanan and D. J. Armstrong, (Harrisbrug, PA: Idea Group Publishing, 2004), pp.

81-108.

[9] S. Pollak, R. Coesemans, W. Daelemans and N.

Lavrac, Pragmatics 21, 674 (2013).

[10] D. Paranyushkin, Prototype Letters 2, 256 (2011).

[11] E. Costenbader and T. W. Valente, Social Networks 25, 283 (2003).

[12] L. C. Freeman, Social Networks 1, 215 (1979).