Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi:10.13106/jafeb.2021.vol8.no3.1205

The Effect of Chairman Tenure on Governance and Earnings Management: A Case Study in Iraq

Mohammed Ghanim AHMED

1, Yuvaraj GANESAN

2, Fathyah HASHIM

3, Abdullah Mohammed SADAA

4Received: November 30, 2020 Revised: February 07, 2021 Accepted: February 16, 2021

Abstract

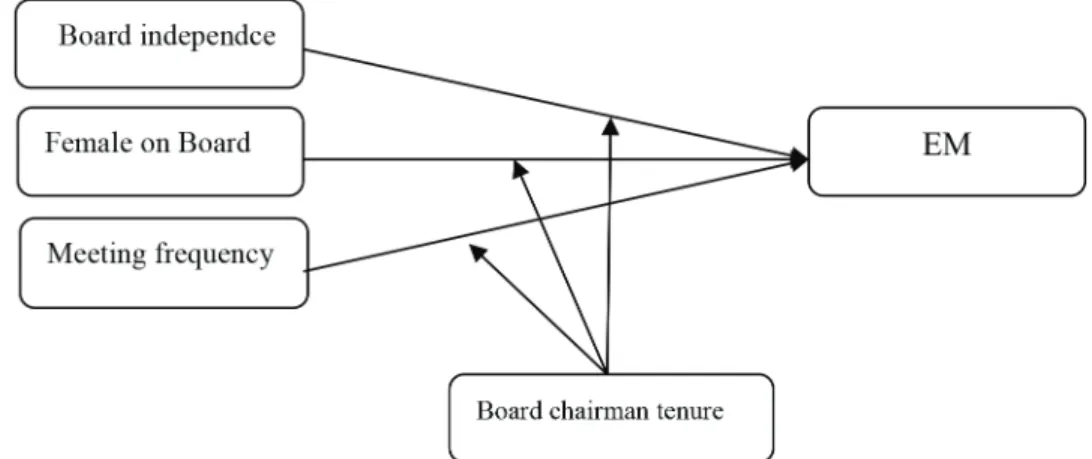

The study’s purpose is to assess how board chairman tenure (BCT) contributes to limiting the earnings management practices (EM) in Iraqi banks. We compare the direct influence of the corporate governance mechanisms (CG) on EM practices and use BCT as a moderator that affects the influence of CG on EM. The sample of the study is the financial’ firms listed on the Iraqi Stock Exchange for the period 2013–2018. Using purposive sampling data was collected from annual reports and data stream. We use the random effect model in panel data regression by using Stata to analyze the data. Findings proved that CG mechanisms insignificantly influence EM, except the meeting frequency was significant.

By contrast, BCT had a positive and considerable influence as the moderating variable between CG and EM. These results suggested that the Chairman’s tenure on the board lead to enhanced governance mechanisms to limit the EM practice in Iraqi financial firms. Accordingly, this study is one of the few studies in the Iraq environment that examine the influence of CG mechanisms on EM practices, in addition to examining the BCT as a moderator between CG and EM, thus, filling the gap in such studies in developing countries.

Keywords: Board Chairman Tenure, Board Meetings Frequency, Females on Board, Board Independence, Beneish Method (M-Score) JEL Classification Code: C58, G20, M21, C12, M14

quality, and rising accruals (Omar et al., 2014; Sadaa et al., 2020). Companies use earnings management to smooth out fluctuations in earnings and present more consistent profits each month, quarter, or year. Management can feel pressure to manage earnings by manipulating the company’s accounting practices to meet financial expectations and keep the company’s stock price up (Alquhaif et al., 2017).

Earnings management, therefore, can be referred to as an act of maximizing the loopholes in the financial reporting laws, to maximize personal, group, or organizational objectives to the detriment of another group of individuals who may be directly or indirectly affected by such decisions (Obigbemi et al., 2016). EM practice often makes financial reporting less quality and reduces shareholders’ confidence in their decision-making (S. U. Hassan & Ahmed, 2012).

Accordingly, EM defines managerial action to decrease (or increase) earnings or revenues for aggressive accounting tactics (Bajra & Cadez, 2018).

The board of directors is responsible for setting ethical standards and values, and ensuring that they are embedded in and become part of the organization. Moreover, the board of directors that are designed to control agency conflict would demand more conservatism because it provides them with early notice of any future losses and assists them in

1

First Author and Corresponding Author. Ph.D. Student, Graduate School of Business, Universiti Sains Malaysia, Malaysia [Postal Address: 11800 Gelugor, Penang, Malaysia]

Email: [email protected]

2

Senior Lecturer, Graduate School of Business, Universiti Sains Malaysia, Malaysia. Email: [email protected]

3

Senior Lecturer, Graduate School of Business, Universiti Sains Malaysia, Malaysia. Email: [email protected]

4

Ph.D. Student, Graduate School of Business, Universiti Sains Malaysia, Malaysia. Email: [email protected]

© Copyright: The Author(s)

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (https://creativecommons.org/licenses/by-nc/4.0/) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.