Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi:10.13106/jafeb.2020.vol7.no7.463

1

First Author and Corresponding Author. School of Finance, Zhongnan University of Economics and Law, China [Postal Address: No. 182, Nanhu Avenue, Donghu New Technology Development Zone, Wuhan City, Hubei Province, 430073, China], Email: [email protected]

2

Henan University, Kaifeng city, Henan Province, China.

Email: zhhwcxf @hotmail.com

3

School of Finance, Zhongnan University of Economics and Law, China. Email: [email protected]

4

School of Finance, Zhongnan University of Economics and Law, China. Email: [email protected]

5

School of Finance, Zhongnan University of Economics and Law, China. Email: [email protected]

6

School of Economics, Zhongnan University of Economics and Law, China. Email: [email protected]

© Copyright: The Author(s)

This is an Open Access article distributed under the terms of the Creative Commons Attribution

Non-Commercial License (http://Creativecommons.org/licenses/by-nc/4.0/) which permits

unrestricted noncommercial use, distribution, and reproduction in any medium, provided the

original work is properly cited.

The Impact of COVID-19 Pandemic on Stock Markets: An Empirical Analysis of World Major Stock Indices

Karamat KHAN

1, Huawei ZHAO

2, Han ZHANG

3, Huilin YANG

4 , Muhammad Haroon SHAH

5, Atif JAHANGER

6

Received: May 03, 2020 Revised: May 24, 2020 Accepted: June 07, 2020

Abstract

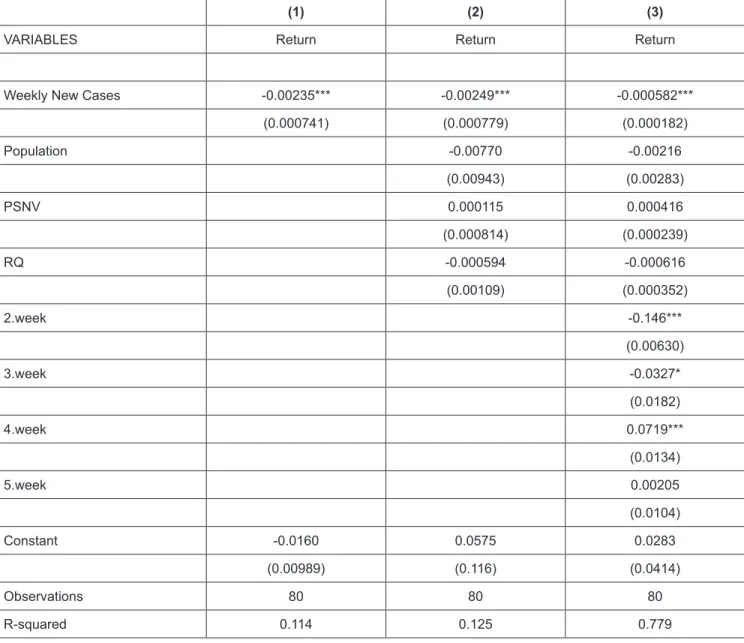

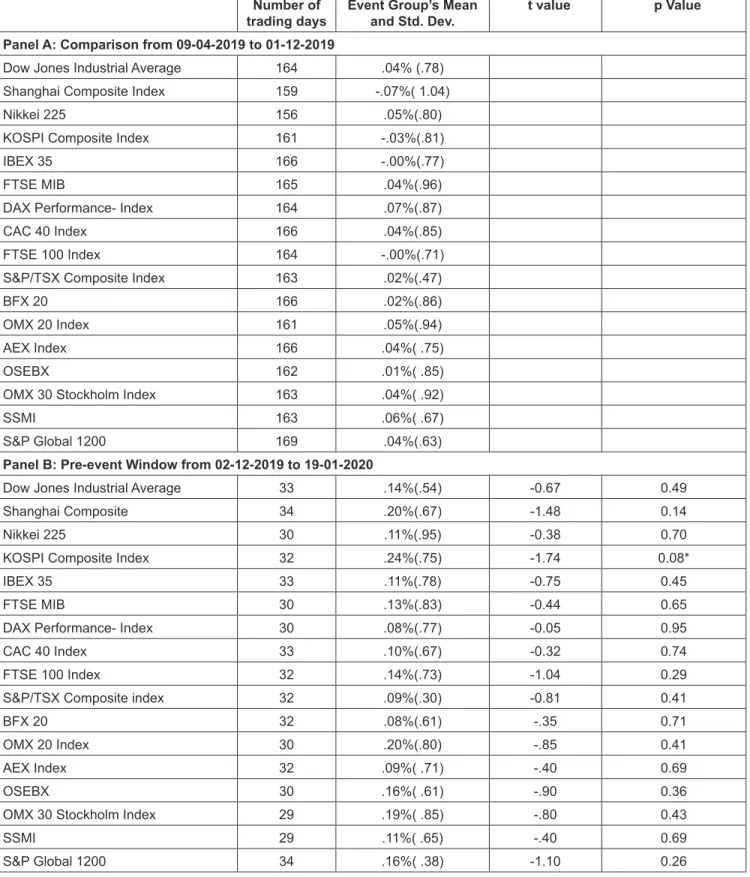

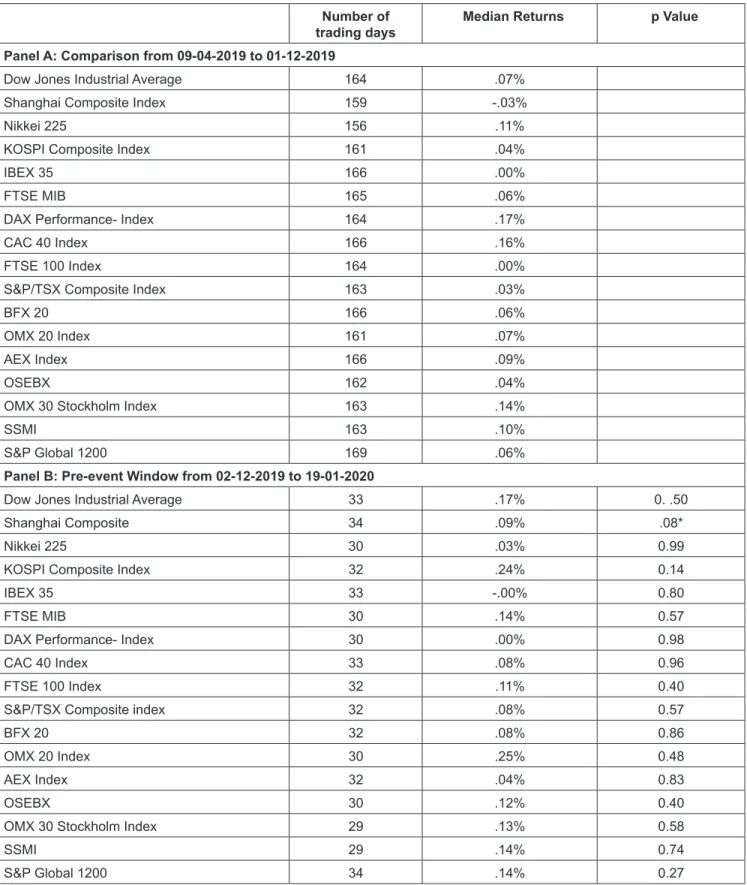

This study aims to investigate the impact of COVID-19 pandemic on the stock markets of sixteen countries. Pooled OLS regression, conventional t-test and Mann-Whitney test are used to estimate the results of the study. We construct a weekly panel data of COVID-19 new cases and stock returns. Pooled OLS estimation result shows that the growth rate of weekly new cases of COVID-19 negatively predicts the return in stock market. Next, the returns on leading stock indices of these countries during the COVID-19 outbreak period are compared with returns during the non-COVID period. We use a t-test and Mann-Whitney test to compare the returns. The results reveal that investors in these countries do not react to the media news of COVID-19 at the early stage of the pandemic. However, once the human-to-human transmissibility had been confirmed, all of the stock market indices negatively reacted to the news in the short- and long-event window.

Interestingly, we noticed that the Shanghai Composite Index, which was severely affected during the short-event window, bounced back during the long-event window. This indicates that the Chinese government’s drastic measures to contain the spread of the pandemic regained the confidence of investors in the Shanghai Stock Market.

Keywords : COVID-19, SARS, Pandemic, Stock Return, New Cases JEL Classification Code: G40, G41, I15, I18

1. Introduction

The future economic impact of the COVID-19 is extremely uncertain due to the spread of the disease as

the death rate, severity of the disease, the response from policymakers, and individual behavior are unknown (Baldwin & Mauro, 2020; McKibbin & Fernando, 2020;

OECD, 2020)this paper explores seven different scenarios of how COVID-19 might evolve in the coming year using a modelling technique developed by Lee and McKibbin (2003.

The disease also added fuel to the uncertainty by causing massive disruption in the lives of people around the world.

The phenomenon, which was not imaginable in the past, is happening in today’s world where more than a third of the world population live life under the curfew or curfews-like situations, fear, panic buying, closure of businesses, factories and educational institutions (Ramelli & Wagner, 2020). The governments are desperately making efforts to contain the health and economic effects of the COVID-19 pandemic (Fiscal Monitor, 2020)

Notwithstanding this situation, the Global Risks Report,

published on 15 of January 2020, said that the top five risks

that the world may face in the long term are all environmental

issues (WEF, 2020). The “infectious disease” because of its

rare occurrence is placed at number 10 in terms of its impact

(albeit the fact that the researchers at the Wuhan Institute of