Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi: 10.13106/jafeb.2016.vol3.no1.5.

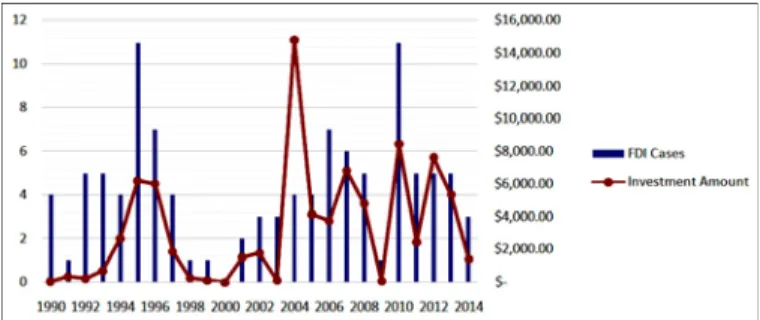

Foreign Direct Investment Projects of Korean Companies

1)

전체 글

1)

수치

관련 문서

Results – Significant factors were identified that determine the flows of bilateral foreign direct investment: GDP home country, GDP host country, real

An Empirical study on the Performance and Entry Strategy for Korean Direct Investment in Mongolia..

This study investigates how the legal provisions contained in Bilateral Investment Treaties (BITs) affect foreign direct investment inflows in OECD countries.. This stands in

This study aims to explore the effects of factors, including leadership style, job satisfaction, and work performance, on the organizational commitment in Foreign Direct

The study aims to assess the impact of foreign direct investment (FDI) and international trade (export and import) on Vietnam's economic growth for the 2000-2018 period..

Because some Asian countries have signed the Free Trade Agreement (FTA) with China, this behavior will affect China’s outward foreign direct investment patterns

The empirical results provide strong statistical evidence that foreign direct investment and human capital has a positive impact on labour productivity in Vietnam in long-term..

Key Words : inward foreign direct investment, investment incentive, industrial electricity price, environmental regulation.. 따라서 아직까지 국내 대기 오염