Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi:10.13106/jafeb.2021.vol8.no6.0347

The Impact of Perceived Risk and Trust on Adoption of Mobile

Money Services: An Empirical Study in Pakistan*

Misbah NOREEN1, Zahiruddin GHAZALI2, Md. Shahin MIA3

Received: February 20, 2021 Revised: April 20, 2021 Accepted: May 02, 2021

Abstract

In Pakistan, usage of mobile money services is very poor due to several reasons including lack of understanding of services, low financial literacy rate, and fear of losing their hard-earned money. Moreover, the association between perceived risk, perceived trust, and mobile money adoption has not yet been examined comprehensively. Therefore, this study aims to assess the impact of perceived risk and perceived trust on the adoption of mobile money services in Pakistan. This study carried out a cross-sectional survey using a standardized questionnaire to collect primary data from the mobile money users in the Punjab Province, Pakistan. Smart-PLS Algorithm and bootstrapping method were employed to analyze the data. The study found that three dimensions of perceived risk, namely, security risk, privacy risk, and financial risk have a significant impact on adoption of mobile money services in Pakistan. Perceived trust was also found to be a significant factor for mobile money adoption in the country. Moreover, the respondents reported that mobile money services save their time and reduce costs in performing financial transactions. The empirical findings of the study might be useful for the policymakers and service providers in enhancing the usage of mobile money services among financially-excluded segments of society.

Keywords: Mobile Money Services, Perceived Risk, Perceived Trust, Pakistan JEL Classification Code: G2, G32, L4, A1

(Alhassan, Li, Reddy, & Duppati, 2020). Mobile money is a prominent emerging fintech service where money is stored on a SIM card (subscriber identity module) for financial transactions, as opposed to the account number given by conventional banking (Ndiwalana, Morawczynski, & Popov, 2010). The emergence of mobile money services plays a significant role to provide access to financial services for financially excluded and underprivileged population (Leong & Sung, 2018). Mobile money in developing countries is a new technological innovation in the financial sector, which is likely to bridge the gap between the accessibility of financial services and financially-excluded communities. Furthermore, mobile money enables consumers to transfer funds, make a deposit, and buy a variety of services and goods by using mobile phones and personal computers (Munyegera & Matsumoto, 2016). According to Morawczynski and Pickens (2009), mobile money is primarily used to transfer money among users without additional exchange of goods or services (Morawczynski, 2008, 2009). Furthermore, mobile money creates advantages for the unbanked population by providing financial access (Munyegera & Matsumoto, 2016).

The rapid increase in the ownership and usage of mobile phones in developing countries shows a greater opportunity

*Acknowledgements:

1The authors of the manuscript would like to thanks the study

participants who provided their time and efforts to participate in the survey.

1 First Author. Ph.D. Scholar, School of Economics, Finance and Banking (SEFB), College of Business (COB), Universiti Utara Malaysia (UUM), Malaysia. Email: [email protected] 2 Corresponding Author. Associate Professor, School of Economics,

Finance and Banking (SEFB), College of Business (COB), Universiti Utara Malaysia (UUM), Malaysia [Postal Address: 06010 Sintok, Kedah, Malaysia] Email: [email protected]

3 Senior Lecturer, School of Economics, Finance and Banking (SEFB), College of Business (COB), Universiti Utara Malaysia (UUM), Malaysia. Email: [email protected]

© Copyright: The Author(s)

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (https://creativecommons.org/licenses/by-nc/4.0/) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.

1. Introduction

Mobile money is an innovative financial service that allows people to execute their financial transactions, like money transfers and bills payment by using means of portable devices such as mobile phones and personal computers

for underprivileged people to be part of digital services specifically mobile money services (Fischer, Blumenstock, & Khan, 2018). Mobile money services also have the potential to improve the living standard of the deprived people. However, in many countries, mobile money uptake still remains low due to several reasons including lack of awareness about its benefits, financial literacy problems, trust, and risk issues (InterMedia, 2013). Particularly, the customers are more concerned about risk and trust issues that arise from the execution of financial transactions via mobile money services (Arslan, Geçti, & Zengin, 2013; McKnight & Chervany, 2001).

According to Yang, Pang, Liu, Yen, and Tarn (2015) perceived ‘risk’ and perceived ‘trust’ remain a central concern for adoption and usage of digital payment systems (Wismantoro, Himawan, & Widiyatmoko, 2020) via mobile money service. When customers experience any potential losses because of innovative technology usage, that may increase their sensitivity for risk. The generated losses may embrace any adverse effects for customers, like financial loss, privacy breach, performance disappointment, mental distress, or discomfort. Perceived risk is that consumers have doubts, reservations, or potential dangers about the consequence of their purchase decision (Arslan et al., 2013). Perceived risk is typically higher for the product given the distinctive characteristics of a service (Carter, Weerakkody, Phillips, & Dwivedi, 2016; De Kerviler, Demoulin, & Zidda, 2016). A possible obstacle for the adoption of financial services could be the potential of risk exposure to mobile money services. The perceived risk linked with the financial service could be security, privacy, and financial risk. Perceived trust also gained separate attention in technology base financial services because of the high level of ambiguity and domain-related risk (Lafraxo, Hadri, Amhal, & Rossafi, 2018). Perceived trust exhibits the willingness of an individual to take risks in order to fulfill a need without prior experience, credible, or meaningful information (McKnight & Chervany, 2001). The significance of perceived trust in digital financial services has been examined comprehensively by a number of previous studies (Connolly & Bannister, 2007; Fisher, Burstein, Lynch, & Lazarenko, 2008; Howard Chen & Corkindale, 2008; Karthikeyan, 2016; Surucu, Yesilada, & Maslakci, 2020).

The usage of mobile money services is very poor in Pakistan, despite the fact that mobile money services are potentially cheaper, more convenient, and time-saving as compared to the traditional channel (Fischer et al., 2018; Tahar, Riyadh, Sofyani, & Purnomo, 2020). Mobile money could have a great impact on financial inclusion in Pakistan. In 2017, only 8.7% of Pakistani people reported having an account at a financial institution, and nearly 48% of financially excluded adults reported owning a mobile phone (Demirguc-Kunt, Klapper, Singer, Ansar, & Hess,

2018). A number of factors were reported as the potential barriers to adoption of mobile money including lack of understanding of services, low financial literacy rate, and fear of losing their hard-earned money (InterMedia, 2013). Moreover, the virtual nature of technology makes people insecure before commencing their financial transactions (Kironget, 2014). However, there is a research gap in assessing the impact of perceived risk and trust in adoption of mobile money services in Pakistan. In other words, the association between perceived risk, perceived trust, and adoption of mobile money service has rarely been examined. Therefore, the aim of this study is to examine the impact of perceived risk and perceived trust on adoption of mobile money services in Pakistan. To the best knowledge of the researchers, this study is the first academic attempt to provide the empirical evidence on the relationship between perceived trust, perceived risk, and mobile money adoption in Pakistan.

2. Literature Review

Mobile money services mean the use of portable devices to access financial services that were previously been provided by the traditional financial institutes (Mothobi & Grzybowski, 2017). Mobile money services provide the facilities to transfers funds and make payments. Mobile money is also known as “cell phone banking and branchless banking” (Diniz, Birochi, & Pozzebon, 2012). The previous traditional banking channel and other automated banking services such as ATMs and e-banking are not satisfying the users’ financial needs. Innovative technologies provide access and availability of financial services, and Internet connection also contributes greatly to increase the popularity of mobile money services. Mobile money service is an innovative technology service that helps to execute low-cost financial transactions. Mobile money services operate by the intersection of financial and telecommunications, various stakeholders from different fields also take part in the process (Donovan, 2012). Among these stakeholders, mobile money agents or companies that are playing the forefront role in the development of mobile money service, play an integral role adoption of mobile money services.

“Trust” and “risk” are widely believed to play significant roles in the adoption of digital services (Safeena, Kammani, & Date, 2018). This is perhaps because online transactions that are performed via smart devices are subject to hacking, financial loss, and are unclear and risky (Shaikh, Glavee-Geo, & Karjaluoto, 2018). Similarly, perceived trust represents a “desire to be vulnerable based on the positive expectation of a future behavior by another party” (Kim, Wang, & Chen, 2018). Concerning innovative financial services, perceived trust denotes “the belief that technological services will save their time and cost and service providers will protect

their hard-earned money and personal information”. An agent delivers financial services to the customer, the trust in the agent plays a great role in consumer’s intention to use mobile money services.

Trust in financial transactions is essential because it can address the fear of losing financial assets, while lack of trust could cause reason to prevent potential users not to engage in innovative financial services particularly mobile money services (Chauhan, 2015). Trust is associated with perceived risk, and lack of trust contributes to increasing the perceived risk (Y. Kim & Peterson, 2017). The risk can be defined as an exposure to a hazard arising from the purchase of a digital financial product or service, like m-banking (Shaikh et al., 2018). In addition, “perceived risk as the amount of risk that unbanked customer observes before using digital financial services particularly mobile money services”. It is difficult to measure the risk objectively; therefore, this study focuses on people’s perception of the risk associated with the digital financial transaction. If the risk is high in any financial transaction, customers may opt out of the transaction or may end up the current exchange of financial products and service (Al-Gahtani, 2011).

Perceived trust and perceived risk are widespread concepts influencing users’ intention for adoption of mobile money services. The administration of money (physical or electronic) would have some advantages for its users. The usage of mobile money services therefore probably brings the benefits and fear of loss as well to users that are either largely deprived or banked. The user’s perception that using digital financial services may expose them to loss of money may also affect the adoption of mobile money services. In addition, mobile money users may also not able to predict the actual outcome accurately or it could be possible that these outcomes could be undesirable (Yang et al., 2015). Furthermore, due to the virtual nature of mobile money services, consumers are not assured that they will receive their cash back when transaction errors occur as it was facilitated in traditional settings.

The theory of planned behavior and theory of reasoned action (Ajzen, 1991) have demonstrated that technology adoption can be determined through “perceived behavioral control, subjective norms, and attitudes”. However, these leading behavioral models rarely address the issues of perceived trust and perceived risk that are the main concern for the adoption of innovative financial services (Yang et al., 2015). Therefore, the current study seeks to bridge that gap by examining customers’ adoption of mobile money services with customers’ perceived trust and perceived risk.

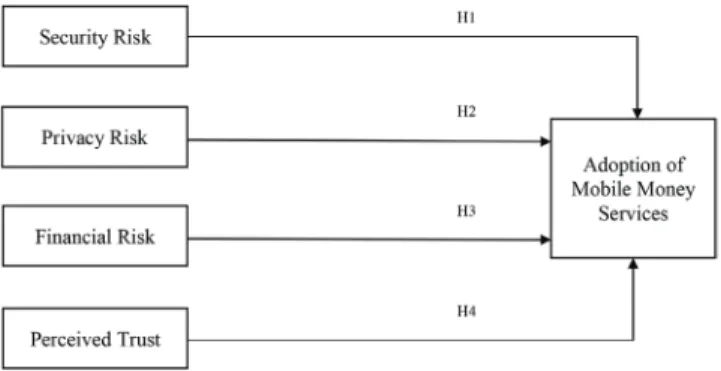

2.1. Research Hypothesis and Model

The research hypothesis and research model were developed based on the review of existing literature and

theories. Security risk “refers to threats that may cause the potential to economic hardship, data issues, or network resources issues in the form of damage, leaks, alteration of data, denial of service, fraud, waste or abuse” (Nofer, 2015). In addition, mobile money users also have fear of identity theft, because it is shown that consumers of digital platforms are very vulnerable to theft (Hille, Walsh, & Cleveland, 2015). Moreover, security risks highlighted such as illegal access to the financial account by using the means of false authentication create security issues for users (Nofer, 2015). According to Jang-Jaccard and Nepal (2014) it is the greatest challenge for the digital financial service provider in winning the customers’ trust related to security issues. Thus, based on the evidence this study formulates the following hypothesis:

H1: Security risk has a significant effect on adoption of

mobile money services.

Privacy risk is “the possibility of losing the personal information while using the financial products and services” (Akturan & Tezcan, 2012). Customers of mobile money services are concerned about their personal information or fear that may be a third party could hack their personal information while conducting digital financial transactions by using the mean of mobile money service (Aboobucker & Bao, 2018). Privacy is particularly critical as consumers can now connect their mobile money accounts to their bank accounts. These risks have a great impact on electronic banking services (Chau & Ngai, 2010). Based on the above discussion, it was hypothesized:

H2: Privacy risk has a significant effect on adoption of

mobile money services.

Financial risk is the assumption that the potential negative effects (danger) of the use of digital goods or services are unknown (Featherman & Pavlou, 2003). Moreover, it is the perception of a user’s potential risk when others know his/her private information (Cox & Rich, 1964; Featherman & Pavlou, 2003; Nyshadham, 2000). When customers experience any potential losses that could be generated because of the uncertainty of using mobile money services, that may increase their perception of risk. The losses may embrace any adverse effects for customers, like a financial loss. Perceived risk is denoted as a critical factor in predicting the adoption of technology. Perceived risk perform a significant role in consumer’s decision to adopt technology (Laforet & Li, 2005; Pavlou, 2003). Therefore, this study developed the following hypothesis:

H3: Financial risk has a significant impact on adoption

Trust plays a central role in adoption (Tobbin & Kuwornu, 2011) of mobile money services. Trust reflects the positive outcome by customer (Song & Zahedi, 2002), in the form to influence the transaction by using mobile money, while lack of trust place an adverse effect on adoption of mobile money services. According to Gefen, Karahanna, and Straub (2003), in a digital environment, clients make rational assessments to ensure their cash value is harmless. It is also evident that consumers don’t want to waste time in regulating their financial transactions and therefore promote digital trade, which saves their transaction time (Kuisma, Laukkanen, & Hiltunen, 2007). Customers prefer their trustworthy sellers (Pavlou, Liang, & Xue, 2007), which indicates that trust in firms will affect customer intention to adopt mobile money services. Thus, based on the existing literature, the following hypothesis was proposed.

H4: Perceived trust has a significant impact on adoption

of mobile money services.

The proposed relationships among the variables in this study can be shown in a graphical format in Figure 1.

3. Research Methodology

3.1. Survey Design, Sampling Technique, and Data Collection

This study conducted a cross-sectional survey in the Punjab province, Pakistan, to collect the primary data. A structured and standardized questionnaire was used to conduct the survey. The questionnaire for this study contained multiple items measures of perceived risk, perceived trust, and mobile money adoption. The targeted population of the study was the users of mobile money services, i.e., people who either pay or receive cash via mobile money services. Krejcie and Morgan (1970) technique was employed to determine the required sample size for this study. According to this technique, the appropriate sample

size is 384 mobile money users in the study area. The study used the “convenience sampling” technique to select the respondents. This technique is easy to use and less expensive for the study area with a very big geographical location. The questionnaires were distributed to the selected respondents and asked them to provide free and fair responses.

3.2. Data Analysis

This study used the partial least squares structural equation modeling (PLS-SEM) approach to analyze the data. Smart PLS 3.0 (Hair, Hult, Ringle, & Sarstedt, 2016) was employed to assess the measurement model and the structural model.

3.3. Measurement of Variables

To measure the constructs of this study, all items were adapted from the existing literature after considering the reliability and validity of specific constructs. Adoption of mobile money service items was adapted from Bongomin, Mpeera Ntayi, and C. Munene (2017); Bongomin and Ntayi (2019). Similarly, items measuring security risk were adapted from Akturan and Tezcan (2012), privacy risk and financial risk from Akturan and Tezcan (2012). The items measuring perceived trust were adapted from G. Kim, Shin, and Lee (2009), Bongomin and Ntayi (2019). All items were measured on a five-point Likert scale (1= strongly disagree, 2 = disagree, 3 = neutral, 4 = agree and 5 = strongly agree).

3.4. Measurement Model

The measurement assessment model is the first step in smart-PLS. This study assessed the measurement model by using three different criteria: reliability, convergent validity, and discriminant validity as recommended by Hair, Sarstedt, Hopkins, and Kuppelwieser (2014). The reliability of the items in this study was assessed by using Cronbach’s alpha and composite reliability. The convergent validity of the constructs was assessed by using the average variance extracted (AVE). Discriminant validity was assessed by the Hetero-Trait and Mono-Trait ratios.

3.5. Structural Model

After assessment of the measurement model, structural models were assessed by using the smart-PLS. PLS Algorithm and bootstrapping approach were used to measure the structural model of the study. The blindfolding process was also used to assess the predictive relevance of the model. Subsequently, path coefficients were used to assess the hypothesis of the study.

4. Results and Discussion

4.1. Assessment of Measurement Model

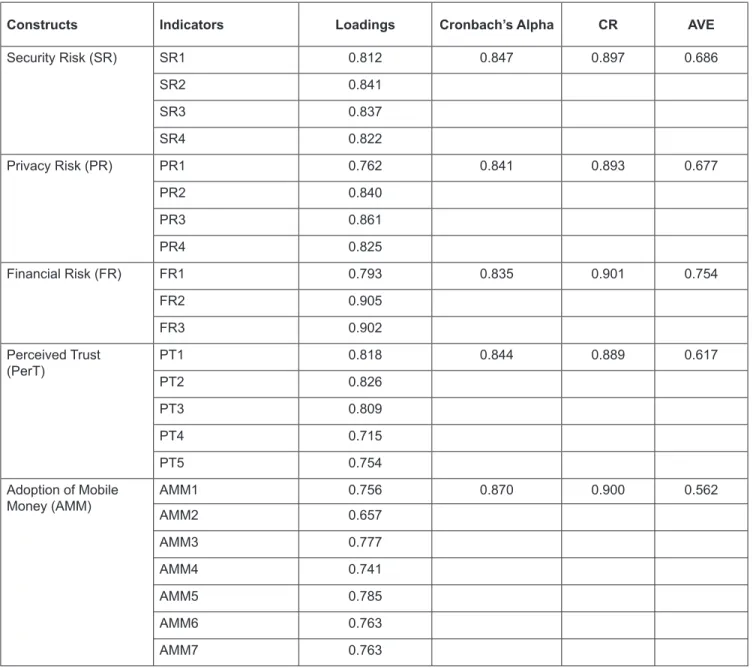

The findings of the measurement model are presented in Table 1. It can be seen that all constructs have successfully met the required criteria of reliability and validity. Cronbach’s alpha and composite reliability of all constructs are greater than 0.7. In addition, the values of AVE are greater than 0.5. The results suggest that all constructs successfully met the criteria of reliability and convergent validity.

Table 2 shows the findings related to discriminant validity. It is important to note that all constructs met the required criteria of discriminant validity. All values among constructs are lower than 0.95. Hence, it is proved that all constructs have met the reliability and validity criteria.

The correlation among the study constructs is presented in Table 3. It can be seen that the correlation value is lower than 0.85 indicating that the variables do not correlate with each other. The findings suggest that the problem of correlation does not exist in this study.

Table 1: Constructs Reliability and Validity

Constructs Indicators Loadings Cronbach’s Alpha CR AVE

Security Risk (SR) SR1 0.812 0.847 0.897 0.686 SR2 0.841 SR3 0.837 SR4 0.822 Privacy Risk (PR) PR1 0.762 0.841 0.893 0.677 PR2 0.840 PR3 0.861 PR4 0.825 Financial Risk (FR) FR1 0.793 0.835 0.901 0.754 FR2 0.905 FR3 0.902 Perceived Trust (PerT) PT1 0.818 0.844 0.889 0.617 PT2 0.826 PT3 0.809 PT4 0.715 PT5 0.754 Adoption of Mobile

Money (AMM) AMM1AMM2 0.7560.657 0.870 0.900 0.562

AMM3 0.777

AMM4 0.741

AMM5 0.785

AMM6 0.763

4.2. Assessment of Structural Model

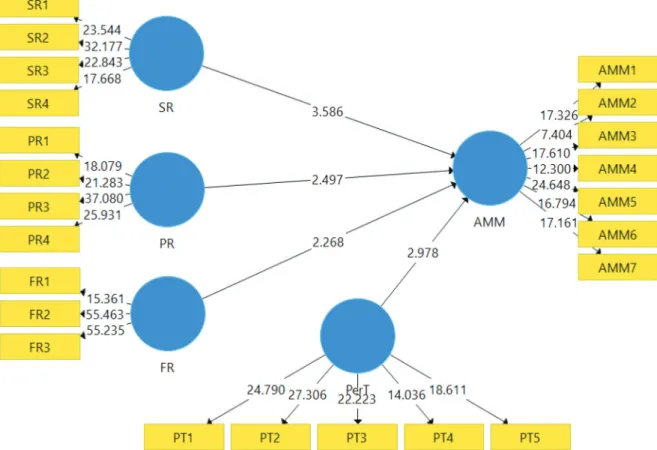

Figure 2 shows the structural path model. The results of the structural model are also presented in Table 4. Four hypotheses of the study show a significant relationship among them.

The relationship between security risk and adoption of mobile money was significant (β = 0.244; p = 0.000). The relationship between privacy risk and adoption of mobile money was also significant (β = 0.142; p = 0.013). In addition, the relationship between financial risk and adoption of mobile money services was found to be significant (β = 0.115; p = 0.023). Moreover, the relationship between perceived trust and adoption of mobile money services was also significant (β = 0.270;

p = 0.003).

Results of the hypothesis testing are presented in Table 4. Hypothesis H1 was supported, that is, security risk impacts the adoption of mobile money service. The results indicate that in Pakistan the security risk for using mobile money services is low. People perceive mobile money services as a

Table 2: Discriminant Validity (HTMT)

AMM FR PR PerT SR AMM FR 0.615 PR 0.609 0.659 PerT 0.708 0.876 0.795 SR 0.665 0.675 0.697 0.782

Table 3: Correlation between Constructs

AMM FR PR PerT SR AMM 1.000 FR 0.529 1.000 PR 0.533 0.552 1.000 PerT 0.612 0.730 0.675 1.000 SR 0.573 0.566 0.595 0.662 1.000

secure way to conduct their financial transactions. Thus, the results of the study were consistent with Hille et al., (2015). Hypothesis H2 also shows a significant relationship among privacy risk and adoption of mobile money. Results show that in Pakistan mobile money services are secure in terms of the private information of mobile money users. Services providers do not disclose the pin code and other personal information of the users.

Hypothesis H3 shows a significant relationship between financial risk and adoption of mobile money. Results of the study indicate that transfer of virtual cash or availing any financial services is secure in Pakistan. There is no financial constraint that exists while using mobile money services in Pakistan. Users find mobile money services secure for the execution of their financial transactions. Hypothesis H4 also shows a significant relationship between perceived trust and adoption of mobile money. Post-usage experience greatly contributes to enhancing the customer trust for the virtual nature of the transaction. Trust in digital services also greatly contributes to reducing the fear of risk for adoption of mobile money services.

5. Conclusion

This study examined the impact of perceived trust and various dimensions of perceived risk on customers’ adoption of mobile money services in Pakistan. The analysis revealed that perceived risk, particularly security risk, privacy risk, and financial risk, have a significant impact on the adoption of mobile money services in the country. The study also found a significant impact of perceived trust on mobile money adoption in Pakistan. Furthermore, the findings of the study confirmed that mobile money service providers in Pakistan work as a safeguard of their customers’ hard-earned money. In addition, mobile money service providers show their highest level of integrity in maintaining the confidentiality of the customers’ personal information as well as mobile money account-related information. On the other hand, customers find mobile money services as a time-savor and cost-effective way for the execution of financial

transactions. This study provided empirical evidence on the relationship between perceived trust, perceived risk, and adoption of mobile money services in Pakistan. The findings of the study might be useful for the regulators and policymakers to design and implement policies to enhance the usage of mobile money services for an inclusive financial system to include the far located and unbanked segments of the society.

References

Aboobucker, I., & Bao, Y. (2018). What obstruct customer acceptance of internet banking? Security and privacy, risk, trust and website usability and the role of moderators. The Journal

of High Technology Management Research, 29(1), 109–123.

https://doi.org/10.1016/j.hitech.2018.04.010

Ajzen, I. (1991). The theory of planned behavior. Organizational

behavior and human decision processes, 50(2), 179–211.

https://doi.org/10.1080/08870446.2011.613995

Akturan, U., & Tezcan, N. (2012). Mobile banking adoption of the youth market: Perceptions and intentions. Marketing

Intelligence & Planning, 30(4), 444–459. https://doi.

org/10.1108/02634501211231928

Al-Gahtani, S. S. (2011). Modeling the electronic transactions acceptance using an extended technology acceptance model.

Applied computing and informatics, 9(1), 47–77. https://doi.

org/10.1016/j.aci.2009.04.001

Alhassan, A., Li, L., Reddy, K., & Duppati, G. (2020). Consumer acceptance and continuance of mobile money. Australasian

Journal of Information Systems, 24. https://doi.org/10.3127/

ajis.v24i0.2579

Arslan, Y., Geçti, F., & Zengin, H. (2013). Examining perceived risk and its influence on attitudes: A study on private label consumers in Turkey. Asian Social Science, 9(4), 158. http:// dx.doi.org/10.5539/ass.v9n4p158

Bongomin, G. O. C., Mpeera Ntayi, J., & C. Munene, J. (2017). Institutional framing and financial inclusion: Testing the mediating effect of financial literacy using SEM bootstrap approach. International Journal of Social Economics, 44(12), 1727–1744. https://doi.org/10.1108/IJSE-02-2015-0032 Table 4: Assessment of Structural Model

Β t-values P-values Confidence Interval Results

2.5% 97.5%

H1 SR → AMM 0.244 3.586 0.000 0.112 0.375 Supported

H2 PR → AMM 0.142 2.497 0.013 0.033 0.256 Supported

H3 FR → AMM 0.115 2.268 0.023 0.015 0.214 Supported

H4 PerT → AMM 0.270 2.978 0.003 0.102 0.455 Supported

R2 = 0.442

Bongomin, G. O. C., & Ntayi, J. (2019). Trust: mediator between mobile money adoption and usage and financial inclusion.

Social Responsibility Journal.

https://doi.org/10.1108/SRJ-01-2019-0011

Carter, L., Weerakkody, V., Phillips, B., & Dwivedi, Y. K. (2016). Citizen adoption of e-government services: Exploring citizen perceptions of online services in the United States and United Kingdom. Information Systems Management, 33(2), 124–140. https://doi.org/10.1080/10580530.2016.1155948

Chau, V. S., & Ngai, L. W. (2010). The youth market for internet banking services: perceptions, attitude and behaviour. Journal of Services Marketing. https://doi. org/10.1108/08876041011017880

Chauhan, S. (2015). Acceptance of mobile money by poor citizens of India: Integrating trust into the technology acceptance model.

info, 17(3), 58–68. https://doi.org/10.1108/info-02-2015-0018

Connolly, R., & Bannister, F. (2007). Consumer trust in Internet shopping in Ireland: towards the development of a more effective trust measurement instrument. Journal of Information

Technology, 22(2), 102–118. https://doi.org/10.1057/palgrave.

jit.2000071

Cox, D. F., & Rich, S. U. (1964). Perceived risk and consumer decision-making—the case of telephone shopping. Journal

of marketing research, 1(4), 32–39. https://doi.org/10.1177%

2F002224376400100405

De Kerviler, G., Demoulin, N. T., & Zidda, P. (2016). Adoption of in-store mobile payment: Are perceived risk and convenience the only drivers? Journal of Retailing and Consumer Services,

31, 334–344. https://doi.org/10.1016/j.jretconser.2016.04.011

Demirguc-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The Global Findex Database 2017: Measuring financial

inclusion and the fintech revolution: The World Bank.

Diniz, E., Birochi, R., & Pozzebon, M. (2012). Triggers and barriers to financial inclusion: The use of ICT-based branchless banking in an Amazon county. Electronic Commerce Research

and Applications, 11(5), 484–494. https://doi.org/10.1016/

j.elerap.2011.07.006

Donovan, K. (2012). Mobile money for financial inclusion.

Information and Communications for development, 61(1),

61–73. https://doi.org/10.1596/978-0-8213-8991-1

Featherman, M. S., & Pavlou, P. A. (2003). Predicting e-services adoption: a perceived risk facets perspective. International

journal of human-computer studies, 59(4), 451–474. https://

doi.org/10.1016/S1071-5819(03)00111-3

Fischer, G., Blumenstock, J., & Khan, A. (2018). Driving usage of mobile money in Pakistan. Available at: https://www.theigc. org/project/driving-usage-of-mobile-money-in-pakistan/. Fisher, J., Burstein, F., Lynch, K., & Lazarenko, K. (2008).

“Usability+ usefulness= trust”: an exploratory study of Australian health web sites. Internet Research, 18(5), 477–498. https://doi.org/10.1108/10662240810912747

Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model. MIS quarterly, 51–90. https://doi.org/10.2307/30036519

Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016). A

primer on partial least squares structural equation modeling (PLS-SEM): Sage publications.

Hair, J. F., Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM).

European business review.

https://doi.org/10.1108/EBR-10-2013-0128

Hille, P., Walsh, G., & Cleveland, M. (2015). Consumer fear of online identity theft: Scale development and validation. Journal

of interactive marketing, 30, 1–19. https://doi.org/10.1016/

j.intmar.2014.10.001

Howard Chen, Y.-H., & Corkindale, D. (2008). Towards an understanding of the behavioral intention to use online news services: An exploratory study. Internet Research, 18(3), 286–312. https://doi.org/10.1108/10662240810883326 InterMedia. (2013). Mobile Money in Pakistan: Use, Barriers and

Opportunities.” Washington, DC: InterMedia. Available at: https://www.intermedia.org/mobile-money-in-pakistan-use-barriers-and-opportunities/.

Jang-Jaccard, J., & Nepal, S. (2014). A survey of emerging threats in cybersecurity. Journal of Computer and System Sciences,

80(5), 973–993. https://doi.org/10.1016/j.jcss.2014.02.005

Karthikeyan, P. (2016). Technology adoption and customer satisfaction in banking technological services. Journal of

Internet Banking and Commerce, 21(3), 1. http://www.

icommercecentral.com/

Kim, Wang, J., & Chen, J. (2018). Mutual trust between leader and subordinate and employee outcomes. Journal of Business

Ethics, 149(4), 945–958.

https://doi.org/10.1007/s10551-016-3093-y

Kim, G., Shin, B., & Lee, H. G. (2009). Understanding dynamics between initial trust and usage intentions of mobile banking.

Information Systems Journal, 19(3), 283–311. https://doi.

org/10.1111/j.1365-2575.2007.00269.x

Kim, Y., & Peterson, R. A. (2017). A Meta-analysis of Online Trust Relationships in E-commerce. Journal of

interactive marketing, 38, 44–54. https://doi.org/10.1016/

j.intmar.2017.01.001

Kironget, L. (2014). Pakistan Mobile Money Analysis. (USAID FIRMS PROJECT), Available at: https://www.academia. edu/15504938/Pakistan_Mobile_Money_Analysis.

Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and psychological

measurement, 30(3), 607–610. https://doi.org/10.1177%

2F001316447003000308

Kuisma, T., Laukkanen, T., & Hiltunen, M. (2007). Mapping the reasons for resistance to Internet banking: A means-end approach. International Journal of Information

Management, 27(2), 75–85. https://doi.org/10.1016/

j.ijinfomgt.2006.08.006

Laforet, S., & Li, X. (2005). Consumers’ attitudes towards online and mobile banking in China. International

Journal of Bank Marketing, 23(5), 362–380. https://doi.

Lafraxo, Y., Hadri, F., Amhal, H., & Rossafi, A. (2018). The Effect

of Trust, Perceived Risk and Security on the Adoption of Mobile Banking in Morocco. Paper presented at the ICEIS (2).

Leong, K., & Sung, A. (2018). FinTech (financial technology): what is it and how to use technologies to create business value in FinTech way? International Journal of Innovation, Management

and Technology, 9(2), 74–78. http://www.ijimt.org/index.

php?m=content&c=index&a=show&catid=93&id=1138 McKnight, D. H., & Chervany, N. L. (2001). Trust and distrust

definitions: One bite at a time Trust in Cyber-societies (pp. 27–54): Springer.

Morawczynski, O. (2008). Surviving in the dual system ‘: How

M-PESA is fostering urban-to-rural remittances in a Kenyan Slum, in. Paper presented at the Proceedings of the IFIP WG.

Morawczynski, O. (2009). Examining the usage and impact of

transformational M-banking in Kenya. Paper presented at the

International Conference on Internationalization, Design and Global Development, Berlin-Heidelberg.

Morawczynski, O., & Pickens, M. (2009). Poor people using mobile financial services: observations on customer usage and impact from M-PESA. http://hdl.handle.net/10986/9492 Mothobi, O., & Grzybowski, L. (2017). Infrastructure deficiencies

and adoption of mobile money in Sub-Saharan Africa.

Information Economics and Policy, 40, 71–79. https://doi.

org/10.1016/j.infoecopol.2017.05.003

Munyegera, G. K., & Matsumoto, T. (2016). Mobile money, remittances, and household welfare: panel evidence from rural Uganda. World Development, 79, 127–137. https://doi. org/10.1016/j.worlddev.2015.11.006

Ndiwalana, A., Morawczynski, O., & Popov, O. (2010). Mobile money use in Uganda: A preliminary study. M4D 2010, 121. http://urn.kb.se/resolve?urn=urn:nbn:se:kau:diva-6480 Nofer, M. (2015). The value of social media for predicting stock

returns: preconditions, instruments and performance analysis:

Springer.

Nyshadham, E. A. (2000). Consumer perceptions of online transaction security-A cognitive explanation of the origins of perception. AMCIS 2000 Proceedings, 111.

Pavlou, P. A. (2003). Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model.

International journal of electronic commerce, 7(3), 101–134.

https://doi.org/10.1080/10864415.2003.11044275

Pavlou, P. A., Liang, H., & Xue, Y. (2007). Understanding and mitigating uncertainty in online exchange relationships: A principal-agent perspective. MIS quarterly, 105–136. https:// doi.org/10.2307/25148783

Safeena, R., Kammani, A., & Date, H. (2018). Exploratory study of internet banking technology adoption Technology adoption and

social issues: Concepts, methodologies, tools, and applications

(pp. 333–355): IGI Global.

Shaikh, A. A., Glavee-Geo, R., & Karjaluoto, H. (2018). How relevant are risk perceptions, effort, and performance expectancy in mobile banking adoption? International Journal

of E-Business Research (IJEBR), 14(2), 39–60. doi: 10.4018/

IJEBR.2018040103

Song, J., & Zahedi, F. (2002). A theoretical framework for the use of web infomediaries. AMCIS 2002 Proceedings, 308.

Surucu, L., Yesilada, F., & Maslakci, A. (2020). Purchasing Intention: A Research on Mobile Phone Usage by Young Adults. The Journal of Asian Finance, Economics and Business

(JAFEB), 7(8), 353–360. https://doi.org/10.13106/jafeb.2020.

vol7.no8.353

Tahar, A., Riyadh, H. A., Sofyani, H., & Purnomo, W. E. (2020). Perceived ease of use, perceived usefulness, perceived security and intention to use e-filing: The role of technology readiness.

The Journal of Asian Finance, Economics, and Business, 7(9),

537–547. https://doi.org/10.13106/jafeb.2020.vol7.no9.537 Tobbin, P., & Kuwornu, J. (2011). Adoption of mobile money

transfer technology: structural equation modeling approach.

European Journal of Business and Management, 3(7), 59–77.

Wismantoro, Y., Himawan, H., & Widiyatmoko, K. (2020). Measuring the Interest of Smartphone Usage by Using Technology Acceptance Model Approach. The Journal of Asian

Finance, Economics, and Business, 7(9), 613–620. https://doi.

org/10.13106/jafeb.2020.vol7.no9.613

Yang, Q., Pang, C., Liu, L., Yen, D. C., & Tarn, J. M. (2015). Exploring consumer perceived risk and trust for online payments: An empirical study in China’s younger generation.

Computers in Human Behavior, 50, 9–24. https://doi.