*정회원: 한세대학교 국제경영학과

**정회원: 경기대학교 경제학과

접수일자: 2017년 12월 26일, 수정완료: 2018년 1월 26일 게재확정일자: 2018년 2월 9일

Received: 26 December, 2017 / Revised: 26 January, 2018 Accepted: 9 February, 2018

*Corresponding Author: [email protected] Dept of Economics, Kyonggi University, Korea https://doi.org/10.7236/JIIBC.2018.18.1.185

JIIBC 2018-1-25

블록체인 기반 서비스 확산을 위한 개선 방안 연구

A Study on Improvement for Service Proliferation Based on Blockchain

유순덕

*, 김기흥

**Soonduck Yoo

*, Kiheung Kim

**요 약 본 연구는 블록체인 기반 서비스의 확산을 위한 방안 연구로서 블록체인 기술에 대한 한계요인과 이를 개선 하는 방안에 대해 전문가의 의견을 수렴하는 델파이 기법으로 연구하였다. 한계요인과 개선방안을 기술, 서비스, 법 제 도 측면으로 분류하였다. 첫째, 기술측면에서 기술 관련 표준화 부재, 통합성 미비, 확장성 미비, 취소, 정정 정책 부재, 거래 검증비용 과다발생, 보안미비를 한계요인으로 제시했다. 이를 개선하기 위해 각 관련 기관이 협력하여 표준화 확 보, 시스템의 통합성 확보 및 확장성 확보, 각 적용되는 데이터에 대한 취소, 정정 정책 수립, 검증비용 효율화와 보안 대비 방안으로 모색하여야 한다. 둘째, 서비스 측면에서 한계요인은 초기단계로 활용성 미비, 보안위협 대응 미비, 전문 인력 부족을 제시하였다. 이에 대한 개선방안으로 다양한 서비스에 적용할 수 있는 지속적인 활용방안에 대한 연구가 이루어져야 하며 서비스에 대한 철저한 보안대응 방안을 준비하고 전문 인력 양성을 통해 시장에서 필요로 하는 인재 를 확보할 수 있어야 한다. 셋째, 법제도 측면은 법적대응 미비, 규제의 불확실성 및 관련 규정미비의 한계점이 있다.

서비스 활성화를 위한 가장 중요한 영역인 법 제도는 정부의 관련 부처에서 법적대응 안 마련, 규제의 명확성 및 대응 방안 수립이 필수적으로 동반되어야 한다. 본 연구는 블록체인 기술 관련 연구에 도움이 될 것으로 기대된다.

Abstract

This study investigates the limitations of blockchain technology and the ways to improve it by using Delphi technique. Limit factors and improvement measures are classified into technology, service, and legal system.First, from a technical point of view, lack of standardization of the technology, insufficiency of integration, lack of scalability, unclear cancellation or correction policy, excessive cost of transaction verification, insufficient personal information protection and not enough to respond to hacking defense were the limiting factors. In order to improve these, the followings; ensuring standardization, securing integration and scalability, establishing cancellation of each applicable data, establishment of correction policy, efficiency of verification cost, the protection of personal information and countermeasure against hacking are provided. The related technology development and countermeasures must be established to effectively introduce the blockchain technology to the market. Second, in the early stage of blockchain service, it showed lack of utilization of the blockchain, security threat, shortage of skilled workers, and lack of legal liability. As a solution to these problems, it is necessary to suggest various applications, against security threat, training professional manpower, and securing legal responsibility. It should also provide a foundation for providing institutionally stable services. Third, from as legal system point of view, inadequate legal compliance, lack of relevant regulation, and uncertainty in the regulation were the limiting factors. Therefore establishing a legal system, which is the most important area for activating the service, should be accompanied by the provision of legal countermeasures, clearness of regulations and measures to be taken by relevant governmental authorities. This study will contribute as a reference for a research, related to the blockchain.

Key Words :

Blockchain, Distributed ledger, Fintech, limitations and improvement, Legal system, Delphi methodⅠ. Introduction

The blockchain is spreading beyond the financial services sector to the manufacturing and distribution sector, the social culture sector, and the public service sector. The financial services sector, a leading leader, can be applied to remittances, currency exchanges, payments, securities, and P2P loans and in the manufacturing and distribution sectors, it can be used for supply chain management and Internet of Things.

In the social and cultural sector, it is possible to use art works, music contents, car sharing, etc. In the public service sector, it can be used for land register, issuance of electronic citizenship, medical records, voting management.

[1]Domestic and foreign blockchain organizations are developing platforms in various ways such as establishing and investing jointly with fintech companies and IT companies, and are proceeding to spread and commercialize blockchain services.

In the early stage of the introduction of the blockchain technology, it is necessary to seek differentiated technology development strategies such as linking with AI and IoT platform in order to lead global market.

This study discusses the limitation factors that are currently emerging for applying the distributed chain technology, which is a blockchain, to various industries, and discusses the improvement ways.

II. Preliminary study and research method

1. Blockchain

Blockchain is a distributed ledger technology in which all members of a network share transaction information between parties.

In order to verify the transaction information, the form of collecting transactions that occurred for 10 minutes is called a block, and conceptually, it is called

a blockchain in the sense that the blocks are sequentially connected.

In detail, a block is a the transaction collected in about 10 minutes and refers to a unit where mining takes place and a blockchain is a connected block to the present.

The blockchain is a ledger that is open to everyone on the network, and the transactions that have occurred so far are recorded in chronological order.

An important feature of the blockchain is that all members of the network jointly record, validate and store transaction information to ensure the authenticity of transaction records without the notarization of a

"trusted third party" such as a central bank or an administrative agency.

It is a highly secure technology because every time a new transaction occurs, each member has to keep track of the ledger being updated at the same time, and therefore all ledgers must be tampered with in order to be hacked.

An example of a well-known blockchain is a bitcoin, a decentralized electronic ledger that records the transaction process of cryptography.

This encrypted transaction record is applied on a computer running blockchain software. Therefore, most of the cipher money including the bitcoin applies the blockchain technique.

[2]2. Preliminary study on blockchain

Aaron Wright and Primavera De Filippi(2015)

explored the benefits and drawbacks of this emerging

decentralized technology and argue that its widespread

deployment will lead to expansion of a new subset of

law, which we term Lex Cryptographia: rules

administered through self-executing smart contracts

and decentralized (autonomous) organizations.

[3]They

discussed that as a result, there will be an increasing

need to focus on how to regulate blockchain technology

and how to shape the creation and deployment of these

emerging decentralized organizations in ways that have

yet to be explored under current legal theory.

In study of Peters, Gareth William and Panayi Efstathios(2015), they provide an overview of the concept of blockchain technology and its potential to disrupt the world of banking through facilitating global money remittance, smart contracts, automated banking ledgers and digital assets. In this regard, we first provide a brief overview of the core aspects of this technology, as well as the second-generation contract-based developments. From there they discussed key issues that must be considered in developing such ledger based technologies in a banking context.

[4]While blockchains have the potential to revolutionize transactions, understanding their limitations is crucial for policymakers and users. Any individual or company that uses a blockchain technology must understand how ultimate control of the nodes is distributed—who will decide the ledger’s accuracy. In many regards, the innovators of the technology intended for decentralization and democratization of transactions, thus revolutionizing the way payments are made, assets are exchanged and contracts are recorded.

[5]The research has shown that this topic is still immature. The results indicate that the Blockchain implementations need to be improved in terms of scalability, latency, throughput, cost-effectiveness, authentication, privacy, security, etc. Accoring to Bojana Koteaka, Elena Karafiloski and Anastas Mishec, they provided an overview of the quality recommendations and solutions for blockchain that could improve the quality of the new blockchain implementations.

[6]According to a study by Kim Hongki (2014), if there is a legal obstacle to the use of domestic virtual currency, the obstacle must be removed and the current regulations should be resiliently interpreted in order to take advantage of the positive aspects of digital virtual currency. In the mid to long term, transaction trends should be identified through reporting and confirmation of transaction details. And he insisted that the financial authorities should have a dedicated organization to

understand the current state of the virtual currency and the market impact.

[7]In the report, "How Will the Emerging Technologies Change Industrial Landscapes: Forecasting the Future and Its Strategic Implications" report, Jang Byeong-yeol and Seol Rae-young (2015)

[8]argued that it is necessary to make a comprehensive and concrete prediction as to what effect the technology will have on the industry, in order to establish a realistic response strategy for the new technology.

In addition, the blockchain technology is replacing traditional financial services by incorporating financial technology and predicts that the impact of Fintech on the financial industry will increase in the future.

3. Purpose and contents of research The purpose of this study is to investigate the limit factors that are currently applied to various industries and to discuss ways to improve them. Therefore, the research problem is defined as "What are the limitation factors for expanding the service based on the blockchain technology and what is the improvement plan?".

4. Research design and the method This study investigates the limit factors for introducing the blockchain into the market and studies on ways to improve it.

Based on expert opinion gathering, we found the causes of limit factors and remedial measures to solve them. Therefore, this study used Delphi technique to derive the opinions of the experts on the limit factors and comprehensively summarize them.

In the case of the Delphi method, according to the previous study, the size of the panel was adopted by more than 10 persons, so this study was conducted by employing 10 experts.

The panel participated in this study was a total of 10

experts including seven experts in the field of

blockchain and three persons in charge of introducing

blockchain service in the business.

An open interview of the panels participated in the research was conducted at Kyonggi University in October.

The first question is what are the limitations of the market introduction of the blockchain technology?. In the case of the second round, the limit factor elements collected in the first round are presented and the improvement plan is discussed.

The following is the summary of the limit ones and improvement factors.

III. Limit factors of blockchain technology

1. Technical field

In terms of technical aspects of the blockchain, there are several limit factors ; (1) lack of standardization, (2) insufficient integration, (3) lack of scalability, (4) unclear cancellation or correction policies, (5) excessive verification costs, (6) insufficient personal information protection, and (7) not enough to respond to hacking defense.

First, there is lack of standardization. The most important problem is that there is no complete standardization at home and abroad considering the compatibility of data and services.

[9]Second, the limitation of the blockchain technology is insufficient integration. As can be seen from the Ripple protocol, blockchain solutions have difficulties in integrating with existing banks and payment systems as well as with each other.

Transitioning to an integrated system requires cooperation and agreement between parties and stakeholders, but the environment for preparing them is insufficient.

[10]Third, there is a lack of scalability. Excessive burden on the network due to the block size enlargement limit can be extended to delays in transaction processing and denial of transactions.

According to TrendBlock, since 2013, the average

block size has increased from 125KB to 425KB and the transaction volume has increased 2.5 times (1 day) to reach the block size limit, 4 times (4*125KB) a day on average.

[11]As of 2017, transactions are limited to 7 transactions per second and 600,000 transactions per day. As of 2015, the volume of transactions is 200,000 per day, which accounts for 33% of the network's speed.

BNY Mellon's Chris Mager argued that it would take seven to 10 years to develop and learn a fully functioning and integrated blockchain based payment system for commercialization or interbank settlement.

[12]Therefore, it is not enough to secure the scalability of the system due to the increase in transactions.

Fourth, there is unclear cancellation or correction policy. One of the important features of a transaction that occurs on a blockchain based network is that it is impossible to cancel or correct a transaction once it has been acknowledged and written to the block. There are currently no specific policies for cancellation and correction in some services.

In this case, if the bitcoin is transferred incorrectly due to a mistake in the transaction, the transaction in the opposite direction must be re-generated to return the bitcoin.

Fifth, the verification costs can be excessive.

Although the possibility of forging and falsification can be significantly reduced through the application of the blockchain technology, there is a problem that it takes a long time to judge the authenticity of the data and the cost associated with the verification may be large. As a typical example, the computing power used in Bitcoin's mining process is estimated to be 20 times the power of Google's entire computer and $ 15 million a day of electricity.

[13]Sixth, personal information protection is insufficient.

One of the main issues is privacy protection, and it is

inherently difficult to guarantee the privacy of

customer data by using the open ledger system, which

is a blockchain technology. This can be mitigated in

any way using a private or authorized blockchain with strict encryption.

Seventh, it is not enough to respond to hacking defenses for individuals who share data. While digital currencies have high stability against data manipulation defenses, there is no way to protect individual users from hacking and data loss.

[15]There is no way to recover a digital call if your private key is lost or stolen by PC or mobile device hacking. However, existing payment services such as credit card and internet banking are equipped with security measures such as official certificates, and procedures for remedy are provided in case of damage such as hacking.

2. Service field

In terms of service, the limit factors of blockchain are (1) lack of utilization of the blockchain, (2) security threat, (3) shortage of skilled workers and (4) lack of legal liability.

First, there is a lack of utilization of the blockchain.

[16]In the early stage of the blockchain, there is a lack of application of related services and lack of various usability. In the case of virtual money, which is a representative example of a blockchain, high price volatility of digital currencies increases transaction costs and serves as a constraint on availability as a means of payment. The limitations of the blockchain based service provide an inactivated environment.

Second, it is a security threat.

[14]. There is a fear of data leakage and exposure in the event of an accident due to lack of security awareness of users and administrators.

Third, there is a shortage of skilled workers.

Blockchain is a newly emerging new technology that lacks professional manpower with high understanding of technical environment of domestic financial industry when developing a blockchain platform.

Fourth, there is a lack of legal liability.

[17]There is a possibility of liability avoidance due to unclear responsibilities and legal role in the condition of

distributed system where financial central organization is difficult to control. Therefore, the subject of legal liability is ambiguous and the rights of the participants are insufficient.

3. Legal system field

Legal system limitations are (1) inadequate legal compliance, (2) lack of relevant regulation, and (3) uncertainty in the regulation.

First, it is inadequate legal compliance.

[18]As can be seen from the representative examples of tax avoidance and tax evasion, it is difficult to comply with the current laws and regulations when introducing a blockchain, and the current regulation is one of the factors impeding the spread of the blockchain.

There is a problem that it is difficult to comply with current laws and regulations such as the Electronic Financial Transactions Act, the Personal Information Protection Act, and the Credit Information Act. In addition, there is no legal system for the current blockchain service, and the interpretation and regulation of related ministries are also inconsistent.

Second, there is a lack of relevant regulations.

[17]In addition to the lack of definitions and regulations on digital currencies, it is difficult to apply the blockchain to the provisions of the Electronic Financial Transactions Act and Supervisory Regulations, the Personal Information Protection Act, and the Credit Information Act, which are based on a centralized computing environment.

As a representative example, the taxation aspect of digital currencies using blockchains is difficult to impose taxes on various transactions at present due to transactions without being controlled by governments and central agencies in each country.

In the case of absorbing the digital money related to the blockchain, there is not enough protection against the problems that arise when using the consortium or private blockchain.

Third, there is uncertainty in the regulation of

related sectors. Blockchains face regulatory uncertainty

and are a lack of a central standard or regulatory organization that monitors and regulates blockchain protocols. It is also difficult to develop regulatory measures because it takes time to develop internationally recognized regulations.

IV. The way to improve the limitations of blockchain technology

1. Technical field

The blockchain technology in Korea that begins to be introduced has a small gap with the technology-dominant country.

In order to lead the global market, it is necessary to seek ways to overcome not only differentiated technology development strategies such as artificial intelligence (AI) and IoT platform but also related limit factors.

In order to overcome the limitations of the above-mentioned blockchain technology, the technical aspect is as follows; (1) ensuring standardization, (2) secure integration, (3) securing scalability, (4) establishing cancellation or correction policies, (5) transaction verification cost efficiency, (6) the protection of personal information, and (7) countermeasure against hacking.

First, it is ensuring standardization. As the number of networks with different business objectives increases, it is necessary to standardize the technology for commercialization of blockchains. Standardization is essential to spread blockchain technology around the world, as IBM has donated Java to the Eclipse community in the past and standardized the platform at the W3C when the Internet first appeared.

The International Organization for Standardization (ISO), the global standardization body, is currently promoting the standardization of the distributed ledge technology, a blockchain technology (2016.12).

In Korea, the Korea Association for ICT promotion and blockchain consortium group in the World Wide

Web Consortium (W3C) are promoting the standardization of related technologies (October 6, 2016).

R3, a US-based FinTech company that has participated in more than 50 financial companies including BOA, Citi and Goldman Sachs, is jointly developing a blockchain standard platform. In addition, it is operating mainly in IT companies such as IBM, Cisco, and Ripple, and is developing standards for open source based blockchain under the Linux Foundation.

Second, there is a need to secure integration. In order to efficiently provide the blockchain service, the system integration must be secured. In order to provide a blockchain based service, it is necessary to establish an environment for integrating or sharing information with related organizations. Therefore, an effective integration method for data management should be provided.

Third, scalability must be secured. It is essential to ensure the scalability of the operating system because continuous data is generated according to transactions.

Therefore, the scalability of the system should be ensured so that the stable service can be operated.

Fourth, cancellation and correction policies should be established. Since there is always a possibility of transaction error or mistake in the capital market, the policy of canceling and correcting the transaction must be included in order for the blockchain technology to be utilized in the capital market.

Fifth, transaction verification cost efficiency is needed. In order to verify the errors and malfunctions of the distributed ledger, it is necessary to establish an effective alternative to the low-cost process.

Sixth, the protection of personal information is required. There is still cyber security issues such as privacy protection that must be solved before the public can utilize personal data in blockchain solutions.

[14]We must thoroughly review the protection of personal information. It should prevent the second accident through exposure of personal information.

Seventh, there is a countermeasure against hacking.

Based on the data stored by each participant, such as the distributor, the second hacking and other related incidents must be prepared to respond to the consumer can use the service.

2. Service field

In order to induce the activation of the blockchain service, it is necessary to prepare for (1) suggesting various application methods, (2) against security threat preparation, (3) training professional manpower, and (4) securing legal responsibility.

In the case of the digital currency, which is a representative example, the above-mentioned improvement plan should be established by preparing the risk management plan based on the price volatility.

First, it suggests various application methods.

Blockchain is emerging as a solution to various problems faced by banks and settlement agencies, and it is necessary to encourage various utilization methods. The blockchain is spreading beyond the financial services sector to the manufacturing, distribution, social-cultural and public service sectors.

Second, it is against security threats. When providing a blockchain based service, thorough countermeasures against security threats must be secured.

Third, it is training professional manpower. The government as well as the private sector should make efforts to train the experts in the blockchain.

Fourth, it is necessary to secure legal responsibility.

The government should take the initiative to make changes in laws and institutions that are appropriate for the environment. In addition, private companies should take measures to play a role and responsibilities for service expansion and competitiveness.

3. Legal system field

The institutional improvement factors are as follows;

(1) preparation of legal responses, (2) preparing of relevant regulations, and (3) clarification of regulations.

First, it is the preparation of legal responses. It is

necessary to establish a preemptive countermeasure by revising the legal system for each type of service in order to ensure stable diffusion of service related to the blockchain.

Companies that are currently commercializing blockchain services are developing blockchain-related technologies in an unstable situation where it is uncertain whether the market is legally viable.

In order for blockchain technology to be used in transactions, settlements, contracts, and information records, it is necessary to prepare measures for applying the electronic financial transaction law, the personal information protection law, and the credit information law.

Second, the relevant regulations should be prepared.

As a representative example, in the case of digital currencies, introduction of necessary regulations should be examined from the viewpoint of consumer protection and anti-money laundering in order to utilize the net function.

Digital currencies, such as Bitcoin, that operate on a public blockchain can be used as an anonymity-based means of money laundering, terrorist financing and tax evasion.

Third, it is necessary to clarify regulations. The current deregulation policy that shifts from the centralized, closed financial ICT supervision system to the distributed open type is required. The current ICT system of financial institutions imposes a centralized management system based on leased lines and closed networks to prevent processing speed, hacking prevention, forgery and counterfeiting illegal transactions, and tax avoidance.

Regulation should be considered in three areas as

follows; (1) regulations to ensure the stability and

reliability of the financial system (macro-prudential

regulations), (2) regulations to ensure the soundness of

financial institutions (micro-prudential regulation) and

(3) Regulation to protect consumers and promote

market competition (regulation of business conduct)

V. Conclusion

With the introduction of the 4th Industrial Revolution era, the blockchain technology has been introduced in various fields and it is emerging as an alternative to solve the problems of current systems.

In the aspect of technology, blockchain is a distributed ledger technology that provides an environment where information is shared among participants.

In this study, the limit factors of blockchain technology and the improvement method are discussed using Delphi technique.

Each limit factor and improvement plan were discussed in terms of technology, service and legal system.

Table 1. Limitations and improvements of blockchain (블록체인의 한계와 개선방안)

Classifi

cation Limitations Improvements

technol ogy

o lack of standardization o insufficient integration o lack of scalability o unclear cancellation or

correction policies o excessive transaction

verification costs o insufficient personal

information protection o not enough to respond to

hacking defense

o ensuring standardization o secure integration o securing scalability o establishing cancellation

or correction policies o transaction verification

cost efficiency o the protection of personal

information

o countermeasure against hacking

service

o lack of utilization of the blockchain

o security threat o shortage of skilled

workers

o lack of legal liability

o suggesting various application methods o against security threat

preparation o training professional

manpower, o securing legal

responsibility.

legal system.

o inadequate legal compliance o lack of relevant

regulation, and o uncertainty in the

regulation

o preparation of legal responses

o preparing of relevant regulations o clarification of

regulations.

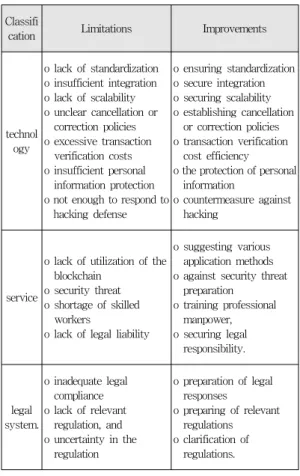

First, from a technical point of view, lack of standardization of the technology, insufficiency of integration, lack of scalability, unclear cancellation or correction policies, excessive cost of transaction verification, insufficient personal information protection and not enough to respond to hacking defense were the limiting factors.

In order to improve these, each related organization should cooperate to ensure standardization, securing integration and scalability, establishing cancellation of each applicable data, establishment of correction policy, efficiency of verification cost, the protection of personal information and countermeasure against hacking.

In addition, although the threat of hacking is evaluated as low technology, the disclosure risk of each information is estimated to be increased, so countermeasures against security threats are essential.

The related technology development and countermeasures must be established to effectively introduce the blockchain technology to the market.

Second, from a service point of view as the early stage of blockchain service, it showed lack of utilization of the blockchain, security threat, shortage of skilled workers, and lack of legal liability.

As a solution to these problem, it is necessary to suggest various application methods, against security threat preparation, training professional manpower, and securing legal responsibility. It should be able to acquire the talents needed in the market by nurturing professional manpower. It should also provide a foundation for providing institutionally stable services.

Third, from as legal system point of view, inadequate legal compliance, lack of relevant regulation, and uncertainty in the regulation were the limiting factors. Therefore establishing a legal system, which is the most important area for activating the service, should be accompanied by the provision of legal countermeasures, clearness of regulations and measures to be taken by relevant governmental authorities.

This study will contribute as a reference for related

research such as the policy related to the blockchain.

In this study, the limit factors of the blockchain were analyzed through the opinion of experts. Therefore, it is necessary to analyze Delphi method or questionnaire in the form of questionnaires through a large number of experts.

Acknowledgement

This work was supported by the GRRC program of Gyonggi province (GRRC 2017 Intelligence information-base security and Network Technology Research)

References

[1] Kim, Sung-Jun, Blockchain Ecosystem Analysis and Implications, KISTEP, ISSN 2508-7622, 2017.

[2] Wikipedia,

https://ko.wikipedia.org/wiki/blockchain.

[3] Wright, Aaron and De Filippi, Primavera, Decentralized Blockchain Technology and the Rise of Lex Cryptographia, SSRN, https://ssrn.com/

abstract=2580664, 2015.

[4] Peters, Gareth William and Panayi, Efstathios, Understanding Modern Banking Ledgers Through Blockchain Technologies: Future of Transaction Processing and Smart Contracts on the Internet of Money, SSRN: https://ssrn.com/abstract=2692487 or http://dx.doi.org/10.2139/ssrn.2692487, 2015.

[5] Koch, Christoffer and Pieters, Gina C., Blockchain Technology Disrupting Traditional Records Systems, Financial Insights – Dallas Federal Reserve Bank. SSRN: https://ssrn.com/abstract=

2997588, 2017.

[6] BOJANA KOTESKA, ELENA KARAFILOSKI

and ANASTAS MISHEV, Blockchain

Implementation Quality Challenges: A Literature Review, CEUR Workshop Proceedings

(http://ceur-ws.org, ISSN 1613-0073), 2017.

[7] Kim Hong Gi, Bitcoin Regulation : Legal and Regulatory Issues of the Virtual Currency System.

Securities Law Research, 15(3), 377-431. 2014.

[8] How Will the Emerging Technologies Change Industrial Landscapes? : Forecasting the Future and Its Strategic Implications, Science and Technology Policy Institute, Vol. 5, 2015.

[9] Kim Hyung Joong, Understanding Blockchain, Software Policy Research, 2017.

[10] Development and understanding of the blockchain technology, FINTECH REPORT, 2016.

[11] Kim, Dong - Sup, Status and Implications of Distributed Director Technology and Digital Credits, 2016.

[12] Chris Mager, Blockchain for finance conference, 2017

[13] Kim, Sung-Joon, Analysis of Blockchain Ecosystem and Implications, Korea Institute of Science & Technology Evaluation and Planning 2017.

[14] Security Technology Research Team, Blockchain Technology and Security Considerations, Financial Security Authority, 2017.

[15] Lee Kyung Hyun, Framework of Integrating Blockchain and Cryptography Technology, Pukyong National University, 2017.

[16] Seo Young Hee, Song Ji Hwan, Gong youngil, Blockchain Technology: Prospect and Implications in Perspective of Industry and Society, SPRI, 2017.

[17] Hong, Seung-pil, Policy Research on the Use of Block Chain in Financial Industry, Financial Security Service, Electronic Finance and Financial Security, No.6, 2016.

[18] Choi, Choong-pil, The Fourth Industrial Revolution

and Block Chain, Korea Institute of Finance, 2016.

저자 소개

유 순 덕(정회원)

∙1991년 2월 : 국민대학교 수학과(학사)

∙1994년 2월 : 연세대학원 수학과 (이 학석사)

∙1995년 12월 : 영국뉴카슬 대학 응용 수학 (석사)

∙2010년 3월 ~ 2013년 2월 : 한세대학교 IT융합박사

∙2013년 9월 ~ 현재 : 한세대학교 조교수

∙관심분야 : 전자금융, 창업 및 벤처, 빅데이터, 정부정책, 개 인정보 및 보안

김 기 흥(정회원)

∙1980년 2월 : 성균관대학교 경제학과 (학사)

∙1984년 6월 : Northeastern University 경제학과(경제학 석사)

․1986년 8월 : Northeastern University 경제학과 (경제학 박사

․1996년 1월 ~ 1997년 1 : Stanford University Asia Pacific Research Institute 객원연구원

․1987년 3월 ~ 현재 : 경기대학교 경제학과 교수

․E-Mail : [email protected]

․관심분야 : 국제경제, 금융, 빅데이터, IOT, 전자금융