Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi:10.13106/jafeb.2021.vol8.no3.0229

Correlation between the Profitability and Working Capital Practices:

A Case Study in the Gulf Cooperation Council

Mohammed Abdul Imran KHAN

1, Md. Shabbir ALAM

2, Ahsan Jamil SYED

3Received: November 20, 2020 Revised: January 25, 2021 Accepted: February 03, 2021

Abstract

The ability of entrepreneurs to arrange working capital is the key to maximizing the profitability of small- and medium-sized enterprises and the wealth of entrepreneurs. The study investigates the correlation between entrepreneurs’ working capital management and the profitability of SMEs listed on six Gulf Cooperation Council (GCC) stock exchanges between 2019 and 2020. The secondary data is collected from the financial statements of SMEs listed on the six GCC stock exchanges. Actual sample for the research study was a total of 136 small- and medium-sized enterprises selected using purposive sampling methods. Four research models were considered in this analysis, all ending up affecting gross profits. The selected entrepreneurial SMEs were listed on six different Gulf Cooperation Council stock exchanges during 2019–2020. The fixed financial assets ratio, financial debt ratio, and company size are used as control variables and data were analyzed using multiple regression. The research results demonstrate that there is a statistically significant negative correlation between profitability measured by gross profit and cash cycle and the components of the cash cycle (including days of accounts receivable and days of inventory).

The study further reveals that there is no significant correlation between gross profit and days of accounts payable.

Keywords: Profitability, Working Capital Management, SMEs, Entrepreneurs, GCC JEL Classification Code: G30, M40, M41, O53

have sufficient cash flow to meet their short-term obligations (Akoto, Dadson, & Peter, 2013). Also, Khan (2016) pointed out that the method of adjusting working capital has a significant impact on the profitability of SMEs. It shows that a certain level of working capital requirements can generate the greatest profit. Zariyawati, Annuar, and Pui-Sanal (2016) also provided support for this. They explained that the goal of working capital management is to ensure that the company can continue by having sufficient cash flow to meet maturity, short-term and short-term operating activities. Developing effective working capital management will also ensure the company’s financial health and help it build its business.

Therefore, it is important to understand the decisive factors of working capital management to ensure that companies can withstand economic fluctuations in the long term.

In this case, the size of SMEs is also very important.

Small- and medium-sized enterprises with low cash sales often encounter cash flow problems, while smaller companies focus on inventory management and conventional credit management (Howorth & Weshead, 2003). On the other hand, high-growth SMEs are unwilling to give credit to their customers. On the contrary, they save a lot of inventory capital.

Having the best inventory level will directly affect working

1

First Author and Corresponding Author. Assistant Professor of Finance & Economics, Dhofar University, Sultanate of Oman [Postal Address: Salalah, Sultanate of Oman] Email: [email protected]

2

Assistant Professor of Finance & Economics, Dhofar University, Sultanate of Oman. Email: [email protected]

3

Associate Professor of Finance & Economics, Dhofar University, Sultanate of Oman. Email: [email protected]

© Copyright: The Author(s)

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (https://creativecommons.org/licenses/by-nc/4.0/) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.

1. Introduction

In the consumer goods sector, many competitors are

offering the same products. Because of the similarity of

the target market, small- and medium-sized enterprises

are required to obtain maximum profits. Every SME has

different marketing and internal strategies to convert

production activities into fast cash flow. One of the strategies

is the management accounting strategy, which focuses on

maintaining an effective level of current assets and current

liabilities to ensure that small and medium-sized enterprises

capital resources and investment in the business cycle.

By managing appropriate expenditures during production and sales, small- and medium-sized enterprises will be able to control cash turnover, debt turnover and inventory turnover to generate maximum profits. Therefore, critical calculations and analysis are essential for understanding market demand and inventory management. Failure to properly perform working capital management will result in inefficiencies in operations, which will make SMEs unable to survive (Khan, Alkathiri, Alhaddad, & Alnajjar, 2021). Based on this background, the author of this article believes that the management of working capital has established a strong correlation between the cash cycle of SMEs and the profitability of SMEs. Therefore, this article aims to study the correlation between SME profits and management in the cash cycle. The main question of this study is to find the correlation between working capital management and the profitability of small- and medium enterprises listed on the GCC stock exchange during 2019–2020.

2. Literature Review

Working capital is the company’s investment in short- term cash assets, treasury securities and accounts receivable (Brigham & Weston, 2010). Sufficient working capital can bring many benefits, such as (1) protecting SMEs from the impact of the crisis caused by the decline in the value of current assets; (2) allowing all debts to be repaid on time; (3) ensuring that, in the face of possible financial difficulties, SME needs credit; (4) providing sufficient inventory; (5) enabling SME to provide its customers with more favorable credit terms;

(6) enabling SME to operate more efficiently because it is not difficult to obtain the required goods or services (Khan, 2019).

However, other working capital management and profit- ability studies have shown different results. Gill, Nahum, and Neil (2010) studied 88 small- and medium-sized companies listed on the New York Stock Exchange from 2005 to 2007 and found that the average payable day, average inventory day, company size, and profitability are not statistically significant.

But notice that there is a negative correlation between accounts receivable and profitability. It suggests that managers can improve the company’s profitability by reducing the number of days of accounts receivable. In theory, companies can maximize profits by controlling cash inflows and outflows and shortening the cash cycle. Brigham and Weston (2010) pointed out that the cash cycle can be shortened by (1) reducing the inventory conversion that can be obtained by processing and selling goods faster, (2) shortening the acceptance period by accelerating invoicing, or (3) extending the cash cycle. Suspend debt by slowing down payments.

The above research results show that the three components of the cash cycle and profitability are inconsistent. Some studies (Iswandi, 2012; Akoto et al., 2013; Gill et al., 2010) have found that cash turnover has no negative and significant

impact on profitability, while other variables (such as AR days, AP days) inventory days affect profitability.

However, other studies have found that there is a strong negative correlation between the cash cycle and company profitability (Lazaridis & Tryfonidis, 2006; Deloof, 2003). This contradiction makes us interested in studying these variables and determining what impact these variables have on the consumer goods industry sector, which has become a basic demand in a society that continues to consume. Considering the important role of working capital in obtaining the best profits for SMEs, we believe that it is necessary to study the impact of working capital management on the profitability of SMEs listed on the Gulf Cooperation Council Exchange.

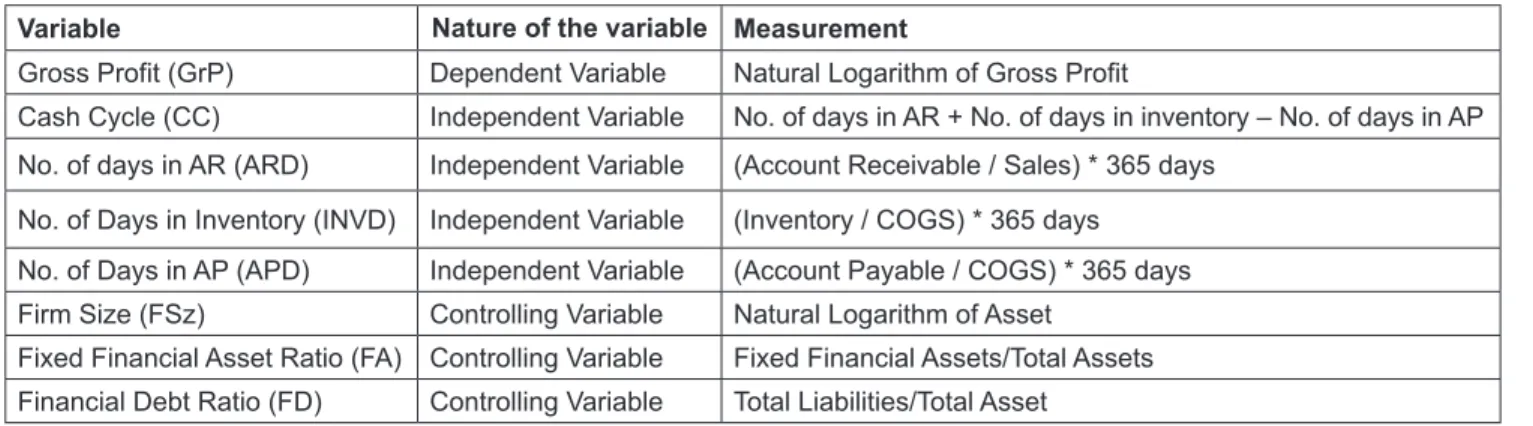

Fixed financial assets ratio, company size (Ln assets), and the financial debt ratio are also considered important for measuring correlation or effect. Therefore, this research aims to determine and analyze the correlation between cash cycle management, accounts receivable management, debt management, and inventory management among the profitability of small- and medium-sized enterprises listed on the six GCC stock exchanges during 2019–2020.

3. Materials and Methods

The secondary data is collected from the financial statements of small- and medium-sized enterprises listed on the six GCC stock exchanges. Actual sample for the research study was a total of 136 small- and medium-sized enterprises selected using purposive sampling methods. The selected entrepreneurial SMEs were listed on six different Gulf Cooperation Council stock exchanges during 2019–2020.

Further, the condition was that these SMEs have not been delisted during 2019–2020, and they did not suffer losses during the research period. The six different GCC stock exchanges referred are, namely, Bahrain Stock Exchange, Kuwait Stock Exchange, Oman-Muscat Stock Market, Qatar-Doha Stock Market, Saudi Arabia Arab-Saudi Stock Exchange (Tadawul), and UAE-Abu Dhabi Stock Exchange.

The descriptive analysis methods were used to analyze

the data and the independent variables determined for this

study are (1) cash cycle, (2) days of accounts receivable,

(3) days of accounts payable, (4) debt turnover rate and

(5) inventory days. The dependent variable of this study

is gross profit, and the independent variable controls are

(1) fixed financial asset ratio, (2) financial debt ratio, and

(3) company size. A multiple regression analysis method is

used, which was previously used to test the hypotheses and is

a requirement for regression analysis testing. The purposive

sampling method is used to select entrepreneurial SMEs

listed on six different Gulf Cooperation Council stock

exchanges during 2019–2020; the condition was that these

SMEs have not been delisted during 2019–2020, and they

did not suffer losses during the research period.

4. Results and Discussions

This study uses multiple regression analysis methods.

This method is consistent with the previous research methods of Lazaridis and Tryfonidis (2006) and Gill et al. (2010). The multiple linear regression analysis models used are:

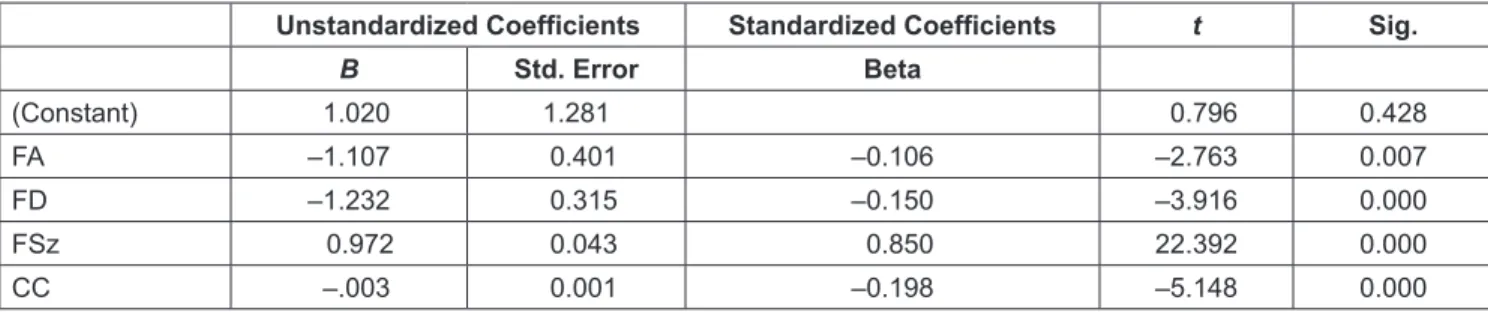

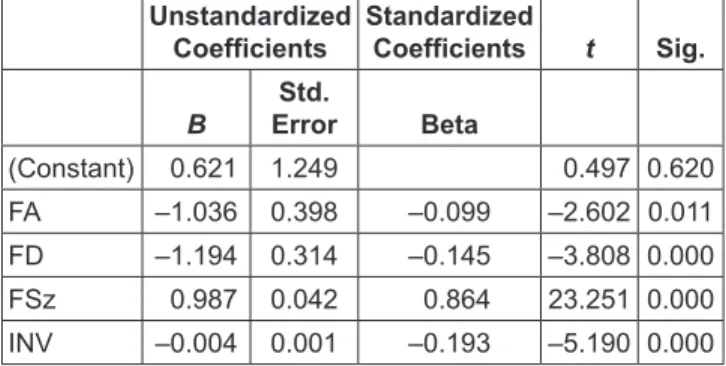

Model 1: GrP = + FA + FD + FSz

0 1 2 3

b b b b

+ CC + random error component Model 2: GrP =

b

4ε

bb b b b

b

0 1 2 3

4